Written by:@longyeyouxin

tutor:@CryptoScott_ETH,@Zou_Block

TL;DR

Ondo Finance is a financial protocol focusing on the RWA track. At this stage, its main business is to tokenize high-quality assets such as U.S. Treasury bonds and money market funds within a compliance framework to facilitate user investment and transactions on the blockchain.

The RWA U.S. debt track where Ondo Finance is located has experienced a 6-fold increase in TVL in the past year and is the main driving force in the RWA industry. Ondo Finance ranks third in the TVL of this track and has a certain first-mover advantage.

The future growth point of Ondo Finance lies in the expansion of the scale of existing products on the one hand, and the launch of other types of RWA products on the other. Its development goal is to become an important bridge connecting the on-chain and off-chain.

The main risk faced by Ondo Finance lies in fierce market competition. The RWA industry is huge but is still in its infancy, and many powerful institutions are vying to enter the market to carve up the market.

The $ONDO token was unlocked for circulation in January 2024, and has experienced a large increase since its listing; however, apart from being used for DAO governance, the token has no other actual use cases, and its future use scenarios are unclear.

About 80% of $ONDO tokens are still in the hands of project parties, the distribution mechanism is still unclear, and there is a large risk of centralization.

1. Introduction to the Ondo Finance project

Ondo Finance is a decentralized institutional-grade financial protocol (Institutional-Grade Finance) that is committed to using blockchain technology to provide institutional-grade financial products and services and create an open, permissionless, decentralized investment bank.

Ondos current core business is to introduce no/low risk, stable interest-earning, and scalable fund products (such as U.S. Treasury bonds, money market funds, etc.) to the blockchain to provide investors on the chain with an alternative to stablecoins. and allows the holder, rather than the issuer, to earn most of the income from the underlying asset.

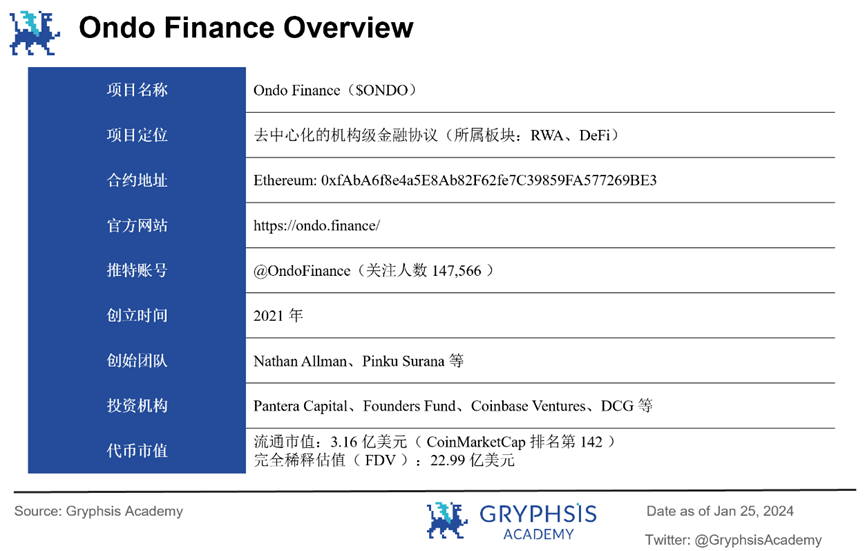

1. Basic information of Ondo Finance project

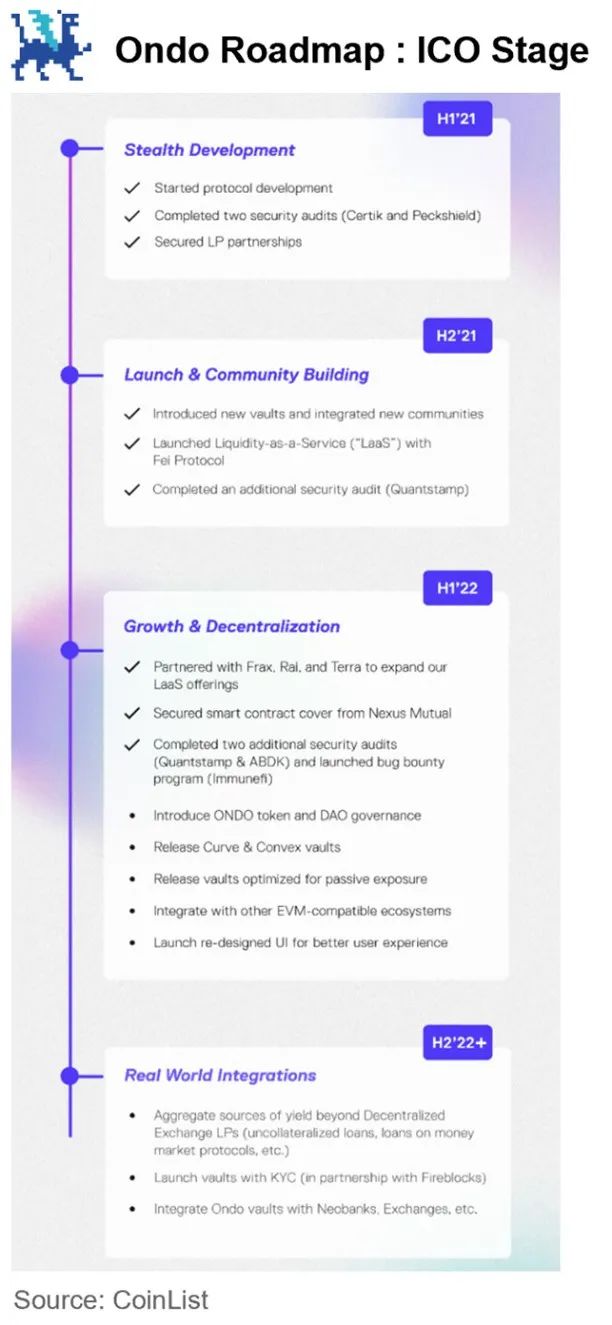

2. Ondo Finance project development history

Ondo Finance focused on the DeFi track when it was first founded. From the end of 2022 to the beginning of 2023, it changed its development route to the RWA track, and achieved good results in 2023. Important points in project development are as follows:

(1) March 2021: The company was founded, focusing on DeFi

Former Goldman Sachs employees Nathan Allman and Pinku Surana co-founded Ondo Finance Inc.. At the beginning, the company was positioned to introduce structured assets with better returns to the DeFi field.

Ondo launched its first product, Ondo Vaults, in August 2021 – a structured finance protocol running on Ethereum. This product allows investors to choose enhanced returns or downside protection when providing liquidity to decentralized exchanges such as Uniswap.

(2) August 2021: Seed round financing

Pantera Capital led the investment, with participation from Genesis, Digital Currency Group, CMS Holdings, CoinFund, Divergence Ventures, Stani Kulechov, Richard Ma, Christy Choi and others. The financing amount of this round is US$4 million, and the token price is 1 ONDO = 0.0057 USD.

At this stage, Ondo describes itself as “the protocol is designed to allow DeFi traders to hedge and exploit risks according to their own wishes.” Ondo allows users to originate risk-isolated, fixed-income loans backed by digital assets. Both lenders and borrowers inject funds into the Vault executed by Ondos smart contract. The Vault provides two options: fixed income to reduce risk and variable income to maximize returns.

(3) Second half of 2021: Launch of LaaS service

Liquidity-as-a-Service (LAAS) can help token issuers increase liquidity on decentralized exchanges. It pairs DAOs with underwriters (stablecoin issuers) to bootstrap highly liquid AMM trading pairs. The DAO provides governance tokens, the underwriters provide stablecoins, and Ondo assists in establishing liquidity pools. The ultimate goal is to help DAO build its own liquidity without having to rely on liquidity mining or market-making companies.

More than 10 DAOs, including NEAR, Synapse, and UMA, as well as underwriters such as Fei, Frax, Terra, and Reflexer, participate in the program. Ondo provides over $210 million in total liquidity (TLP) between the community and LaaS Vault.

(4) April 2022: Series A financing

Pantera Capital and Founders Fund led the investment, with participation from Wintermute, Tiger Global Management, Steel Perlot, GoldenTree Asset Management, Flow Traders, Coinbase Ventures and others. The financing amount of this round is US$20 million, and the token price is 1 ONDO = 0.0285 USD.

At this stage, Ondo describes itself as “the protocol provides structured investment products built on decentralized exchanges.” In addition to the treasury investment mentioned in the seed round of financing in August 2021, Ondo at this stage also provides LaaS to DAO.

(5) May 2022: ICO financing

Ondo completed ICO financing on the CoinList platform. 3 million ONDO will be sold at a price of US$0.03, with a lock-up period of 1 year, and will be released linearly within 18 months after unlocking; 17 million ONDO will be sold at a price of US$0.055, with a lock-up period of 1 year, and will be released within 6 months after unlocking Linear release. The financing amount of this round is US$10.25 million. For most public investors: 1 ONDO = 0.055 USD.

At this stage, Ondo describes itself as providing services and connections to various stakeholders in the emerging DeFi ecosystem - including DAOs, institutions and individuals. At that time, the project roadmap announced by the Ondo team was as follows:

(6) January-February 2023: Abandon Vaults and LaaS, transform into RWA track

With the compression of DeFi yields in 2022, the Ondo team decided to eliminate Vaults and LaaS (collectively referred to as Ondo V1) and focus on the development of the next generation protocol. Ondo V2 includes Ondo Funds and Flux Finance at launch.

Ondo has modified its positioning to build the next generation of financial infrastructure to improve market efficiency, transparency and accessibility. It has launched two tokenized financial products, USDY and OUSG, and transformed into a member of the RWA track.

(7) January 2024: ONDO tokens will be unlocked and circulated

After on-chain community voting, ONDO tokens were unlocked for circulation on January 18, 2024. After being unlocked, they experienced a large increase, and the price once exceeded 0.3 U. Coinbase also announced that ONDO will be included in the currency listing roadmap.

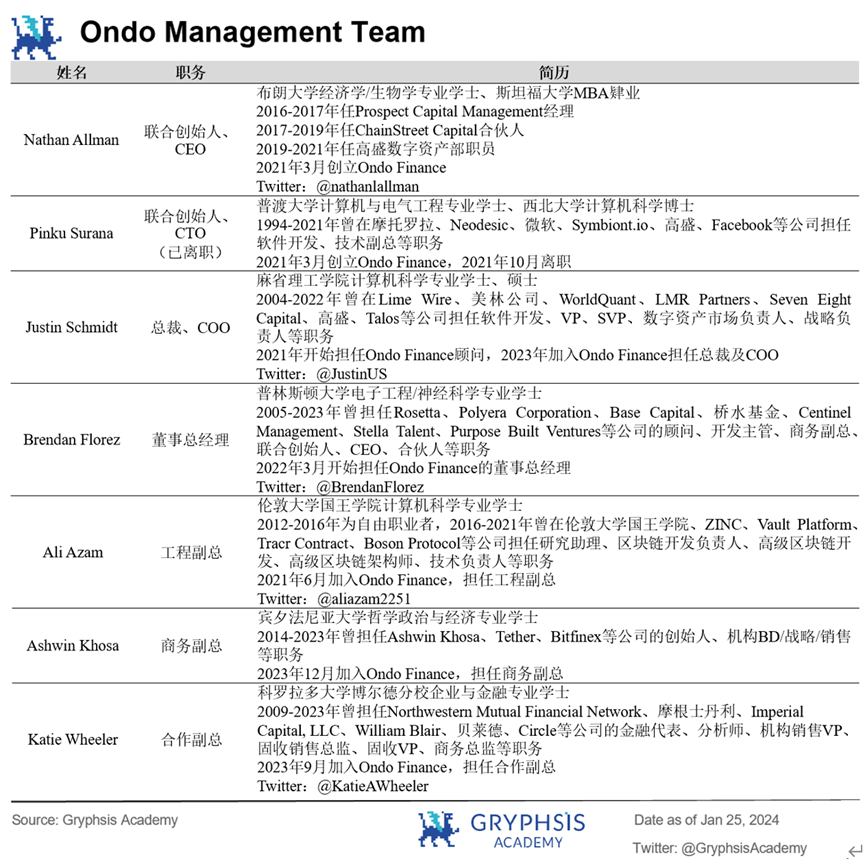

3. Ondo Finance core team background

2. Ondo Finance business model

Ondo Finance consists of two main divisions: the Asset Management Division, which is responsible for the creation and management of tokenized financial products, and the Second Division, which is responsible for the development of decentralized financial protocols.

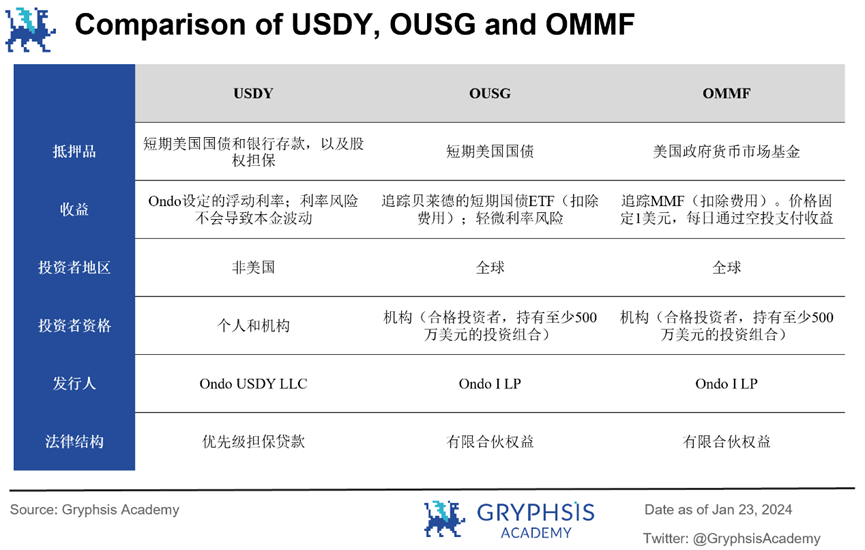

Investors can invest in products launched by Ondo by connecting a digital wallet. Ondo’s current tokenized financial products include the interest-bearing stablecoin Ondo US Dollar Yield Token ($USDY) and the tokenized U.S. bond fund Short-Term US Government Treasuries ($OUSG), and is planning to launch a tokenized money market fund. Ondo US Money Markets ($OMMF). Purchase of the above products requires KYC verification.

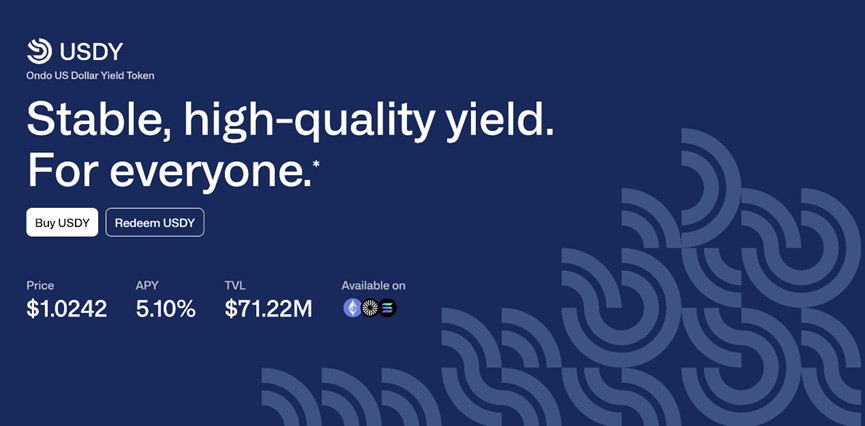

1. Interest-bearing stable currency USDY

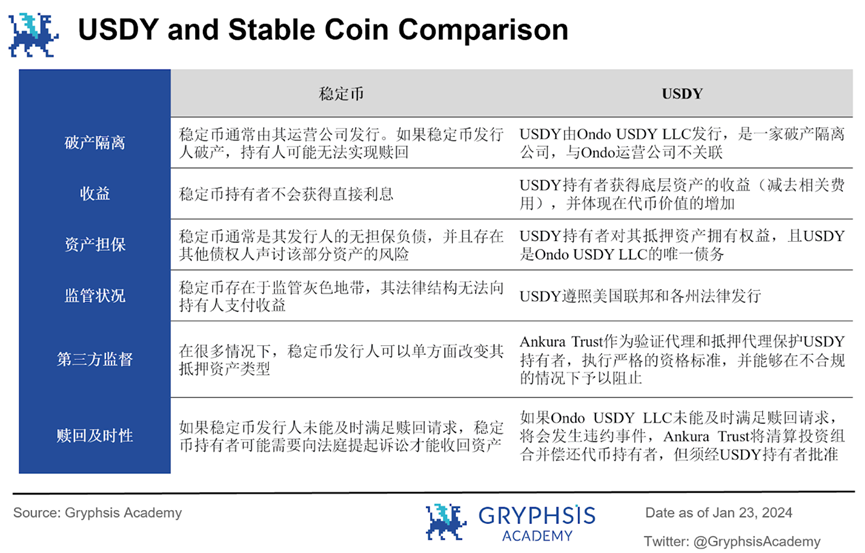

USDY is a tokenized note backed by short-term U.S. Treasury securities and demand bank deposits, available for purchase by non-U.S. individual and institutional investors. After investing, investors will receive a token certificate (Token Certificate) and receive USDY in 40-50 days. After receiving USDY, investors can transfer it on the chain for free. In terms of legal structure, USDY is issued by Ondo USDY LLC, a bankruptcy isolation company, which can isolate Ondos own operating risks to a certain extent.

As of January 23, 2024, the total locked value (TVL) of USDY is approximately US$71.22 million.

(1) Yield and expenses

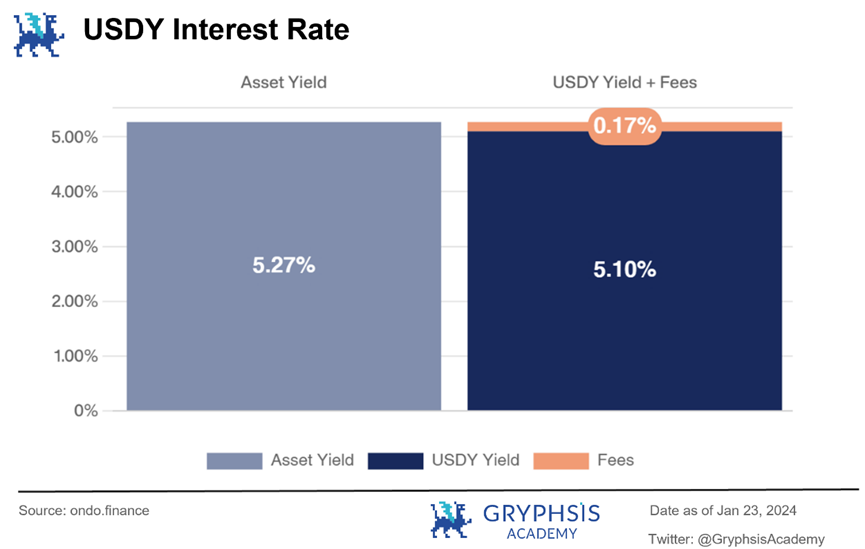

The annualized yield (APY) provided by USDY is adjusted by Ondo every month based on actual conditions. As of January 23, 2024, the APY of USDY is 5.10%. The APY of the underlying assets (i.e., a portfolio of U.S. Treasury bonds and bank deposits) is approximately 5.27%, and the fee charged by Ondo is 0.17%.

In addition to charging fees through the spread mentioned above, Ondo also charges a 0.2% fee on redemptions. In addition, for investments or redemptions under US$100,000, investors will be responsible for wire transfer/currency transfer fees if made by bank wire (these fees are charged by the service provider and not Ondo). But for investments or redemptions above $100,000, Ondo will pay these fees on behalf of the investor.

In addition, Ondo also specifically reminds investors that USDY is structured so that investors will not trigger U.S. federal income tax obligations.

(2) Token price

The token price of USDY is calculated based on the token price on the first working day of the month and the token yield for that month. For example: If the USDY price on June 1st is US$100.00000000 and the APY in June is 4.00000000%, the USDY price on June 3rd will be:

The price of USDY as of January 25, 2024 is $1.0242.

(3) Mortgage guarantee mechanism

USDY is issued by Ondo USDY LLC, an independent legal entity, and is managed by an independent board of directors. It has independent books and accounts, and its assets are isolated from Ondo Finance, Inc.

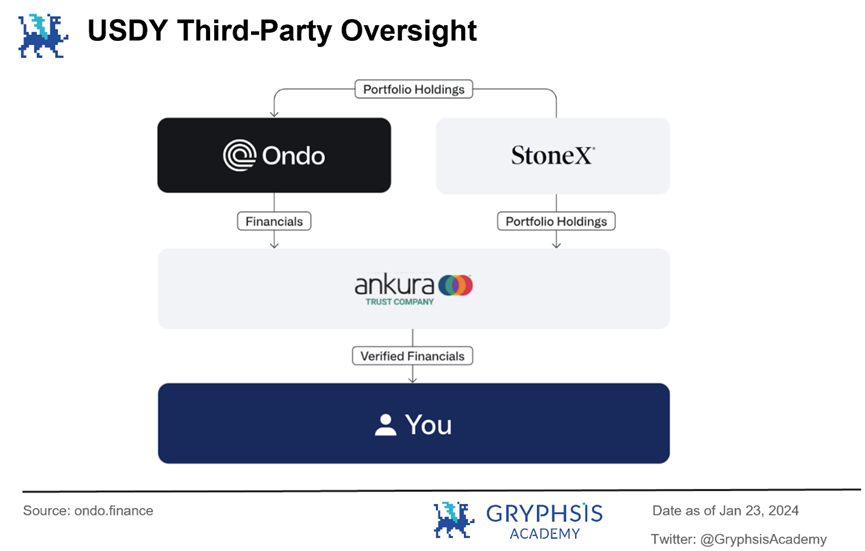

USDY serves as senior debt secured by bank demand deposits and short-term U.S. Treasury securities, which Ondo overcollateralizes, providing a 3% initial loss position to absorb short-term fluctuations in U.S. Treasury prices. In other words, for every $100 worth of USDY issued, there are at least $103 worth of bank deposits and U.S. Treasury bonds as guarantees. In addition, Ankura Trust, acting as the security agent, will provide daily transparency reports containing detailed asset holdings.

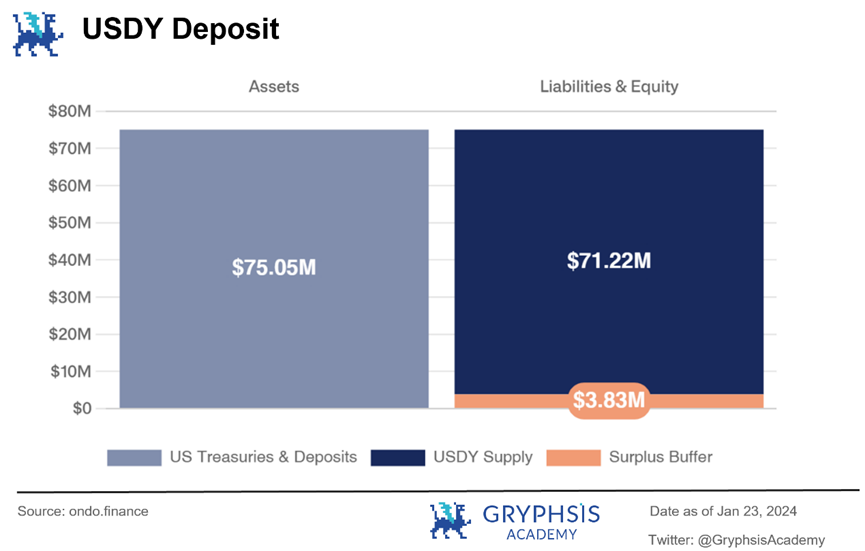

As of January 23, 2024, USDYs total locked value (TVL) is approximately US$71.22 million, the collateral value is approximately US$75.05 million, the over-collateralization amount is US$3.83 million, and the over-collateralization rate is 5.38%.

(4) Investment and custody

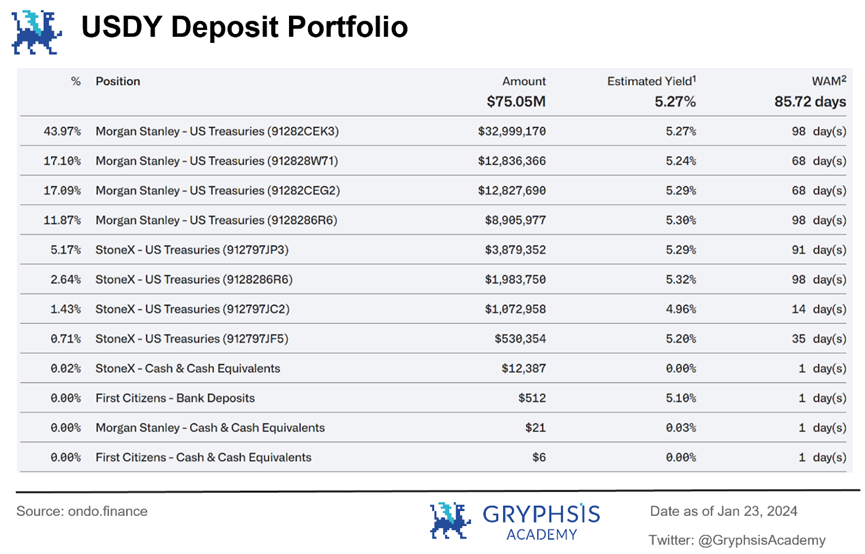

In terms of investment, Ondo said that for USDYs collateral, its goal is to maintain 65% of bank deposits and 35% of short-term government bond allocation, and not invest in any other assets.

In terms of custody, U.S. Treasury bonds will be deposited at Morgan Stanley and StoneX, and these U.S. Treasury bonds will not be remortgaged; bank deposits will be deposited at Morgan Stanley and First Citizens Bank. Ondo also regularly announces its collateral composition on its official website.

(5) Comparison between USDY and stablecoins

USDY is essentially not a traditional stable currency, but a tokenized guaranteed instrument. The specific comparison between USDY and traditional stablecoins is as follows:

2. Tokenized U.S. Bond Fund OUSG

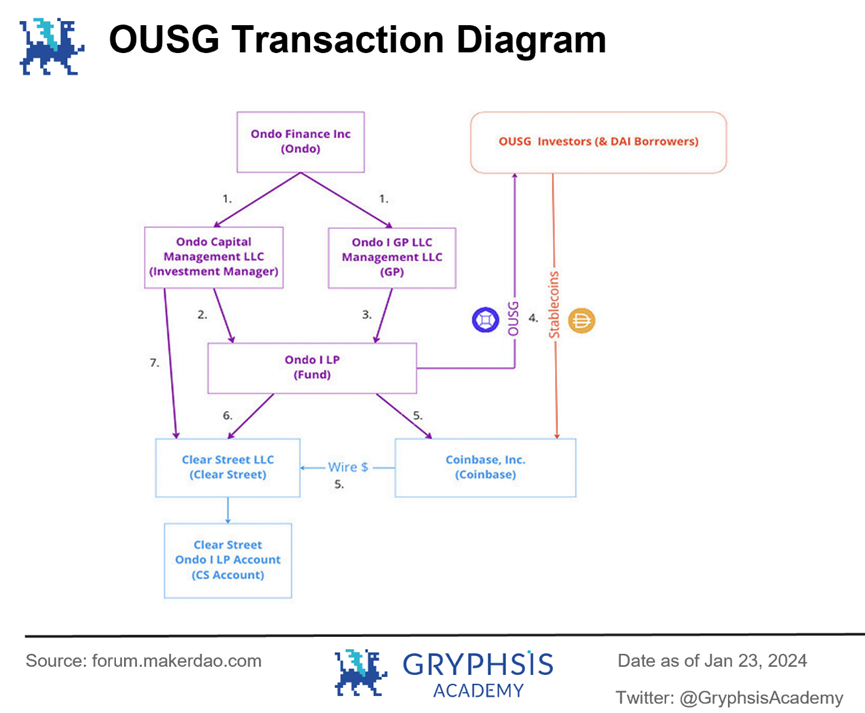

OUSG is a tokenized U.S. Treasury bond fund that aims to provide a liquid exposure to the purchase of short-term U.S. Treasury bond ETFs. Global investors can purchase OUSG using USDC or US dollars, and the minimum investment amount is 100,000 USDC. In terms of legal structure, OUSG is issued by Ondo I LP, a partnership registered in Delaware, USA, and follows a standard fund structure.

As of January 23, 2024, the total locked value (TVL) of OUSG is approximately US$117 million.

(1) Investment and custody

The vast majority of the portfolio will be invested in BlackRocks iShares Short-term Treasury Bond ETF (NASDAQ: SHV ), with a small holding of USDC and U.S. dollars maintaining liquidity.

Ondo I GP is the general partner (GP) of Ondo I LP; Ondo Capital Management acts as an investment manager to assist GP in providing management services; Ondo Finance itself provides technical services to tokenize the fund; Clear Street serves as a securities brokerage company and qualified custody People are responsible for executing fund trading instructions (i.e. buying and selling ETFs); Coinbase acts as a cryptocurrency custodian and brokerage company that holds on-chain assets (USDC).

The relationship between the above subjects can be referred to the following figure:

(2) Yield and expenses

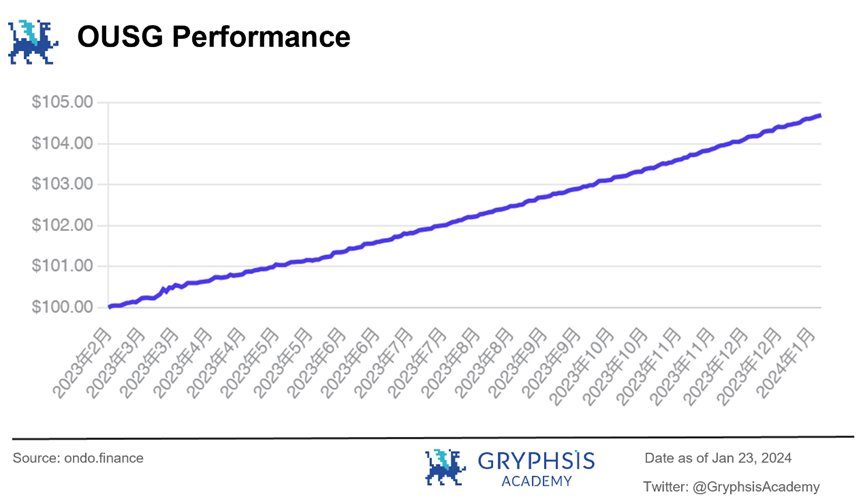

As of January 23, 2024, OUSG provided an annualized yield (APY) of 4.73%.

For the underlying ETF assets, according to the updated data on January 19, 2024: its worst estimated return (YTW) is 5.03%, the 30-day SEC return is 5.15%, the total asset size is US$18.34 billion, and the daily turnover to $235 million.

In terms of fees: Ondo charges a management fee of 0.15%; service providers such as Nav Consulting charge a service fee of up to 0.15% (this proportion will decrease as TVL increases); ETF management fees are 0.15%.

Since its issuance in February 2023, the price of OUSG has continued to move higher as gains are realized, with the current price being 1 OUSG = $104.70.

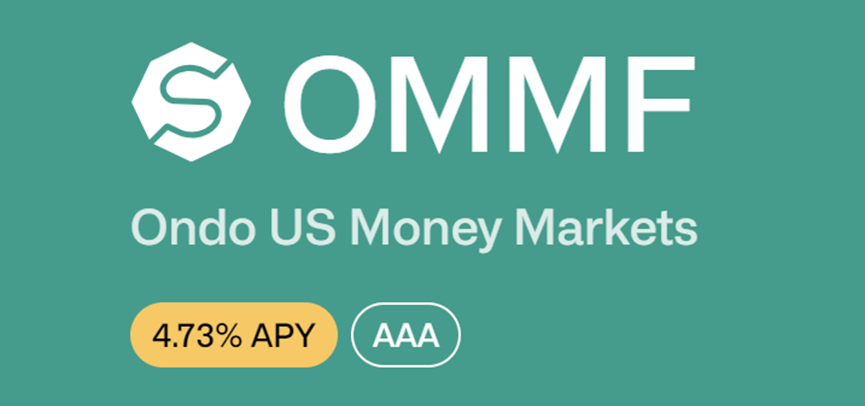

3. Tokenized Money Market Fund OMMF

The upcoming OMMF is a tokenized money market fund designed to provide liquidity exposure to purchases of U.S. money market funds. Similar to OUSG, global investors can purchase OMMF using USDC or US dollars, and the minimum investment amount is also 100,000 USDC.

(1) Investment portfolio

The vast majority of the portfolio will be invested in money market funds (MMF), with a small portion of USDC and US dollars held to maintain liquidity.

(2) Yield and expenses

OMMF has not yet been issued, and the annualized yield (APY) shown on its official website is 4.73%.

Future earnings will be airdropped daily to token holders in the form of new tokens, and OMMF tokens will always be purchased and exchanged for $1.

Ondo has also yet to announce the underlying MMF asset class.

In terms of fees: Ondo charges a management fee of 0.15%; service providers such as Nav Consulting charge a service fee of up to 0.15% (this proportion will decrease as TVL increases); MMF management fees have not yet been announced.

4. Comparison of three tokenized financial products

The main differences between the three tokenized financial products USDY, OUSG and OMMF include:

OUSG and OMMF represent equity/shares held in Treasury bonds and money market funds respectively, while USDY is an interest-bearing note.

OUSG and USDY are total return instruments: any interest paid on the underlying asset is reinvested, such that the value of these tokens typically increases over time. Any interest paid in OMMF is regularly paid to investors in the form of additional OMMF tokens, keeping the value of OMMF close to $1.

OUSG and OMMF are available for purchase by qualified investors around the world; USDY is only available to investors in qualified regions, but does not require investor certification.

OUSG and OMMF can be traded on the secondary market at any time; USDY has a lock-up period, but can be traded freely after the lock-up period.

The specific comparison table is as follows:

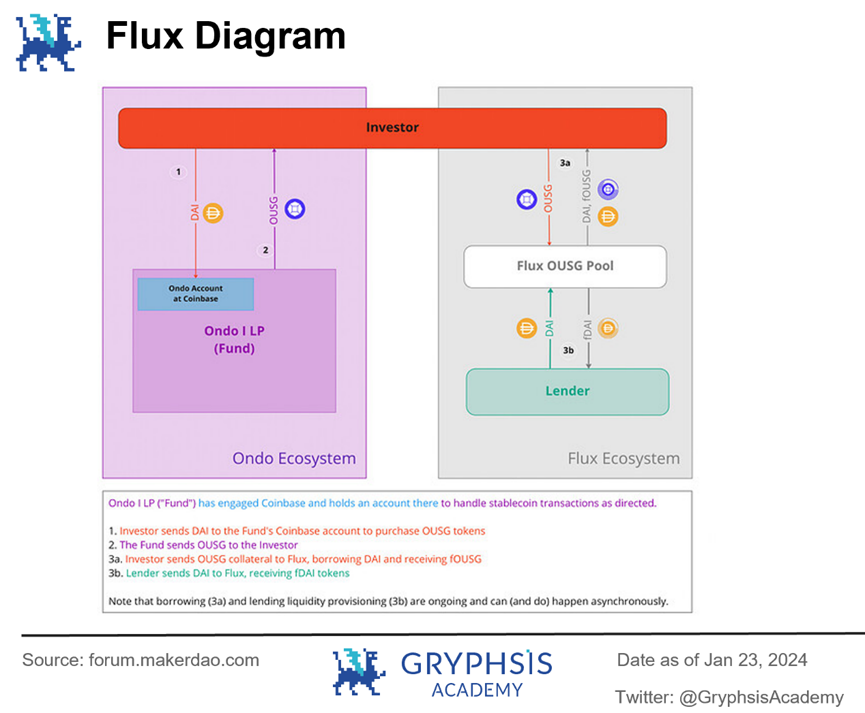

5、Flux Finance

Due to regulatory compliance reasons, some of Ondos products are only available to KYC licensed customers. Therefore, Ondo cooperates with the back-end DeFi protocol Flux Finance to provide stablecoin mortgage lending services for tokens that require permissioned investment, such as OUSG, to achieve permissionless participation in the back-end of the protocol.

Flux Finance is a decentralized lending protocol launched by the Ondo team based on Compound V2. The protocol is basically similar to Compound. The protocol allows users to borrow and lend stablecoins backed by high-quality collateral such as OUSG. Currently, Ondo has sold the agreement to Ondo Foundation (formerly known as Neptune Foundation).

The interaction between Ondo and Flux ecosystem can be seen in the figure below:

3. Ondo Finance project prospects

1. Industry analysis

Ondo Finance is currently an important member of the RWA circuit.

RWA (Real World Assets) refers to the tokenization of real assets. By putting real world assets on the chain, token holders have ownership of the corresponding assets in the real world and can make loans on the chain. , leasing, buying and selling and other transactions.

RWA covers a wide range of assets, including sovereign currencies, bonds, stocks, real estate, commodities (such as gold) and other types of assets. As a high-quality asset with excellent credit and liquidity, U.S. Treasury bonds have become the main driver of the large-scale expansion of the RWA track in recent years.

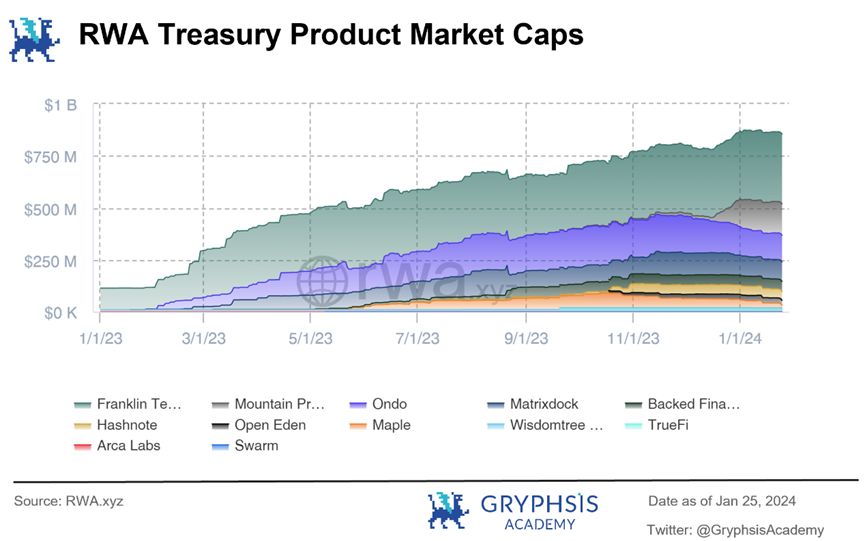

According to data from RWA.xyz, the total market value of RWA U.S. Treasury bonds was only US$114 million on January 1, 2023, and reached US$855 million on January 25, 2024, an increase of 6 times in just one year. (And the above amount does not include MakerDAOs use of more than 2 billion U.S. dollars in U.S. debt as collateral for $DAI).

Among them, Ondo’s RWA U.S. debt market size reached US$128 million, ranking third in the market, second only to Franklin Templeton Benji Investments (US$336 million) and Mountain Protocol (US$151 million).

U.S. bonds have high credit and good yields. Especially in the context of the poor global economic situation in 2023 and the Federal Reserves multiple interest rate hikes, many investors choose to buy U.S. bonds to obtain better risk-free returns. But one of the pain points of investing in U.S. bonds is the high investment.

Even for U.S. citizens, the cumbersome KYC and account opening procedures are enough to shut out most people, and it is even more difficult for non-U.S. citizens. Therefore, how to introduce U.S. debt into the blockchain and lower investment thresholds in compliance with regulations is the most concerning issue for many RWA protocols.

One of Ondo’s current successes is that it has initially solved the compliance issue of U.S. debt on-chain within the existing legal framework of the United States, allowing participants in the RWA U.S. debt market (including investors, fund managers, custodian banks, brokers, etc. All parties) can agree on the operating rules of USDY and OUSG and have actually participated.

It can be said that Ondo has seized the opportunity in the RWA U.S. bond market. In the future, Ondo can leverage this advantage to continue to expand tokenization paths for other asset classes.

2. Competitors

Ondo Finance’s main competitors in the RWA industry include Franklin Templeton, Mountain Protocol, etc. A brief introduction to each competitor is as follows:

(1)Franklin Templeton

Franklin Templeton (Franklin Templeton Fund Group) is the worlds leading asset management company, with a history of more than 70 years and over one trillion US dollars in assets under management. As a giant in the traditional financial field, Franklin Templeton has been very actively involved in the cryptocurrency industry, and his application for a spot Bitcoin ETF (EZBC) was approved by the US SEC in January this year.

As early as April 2021, Franklin Templeton had launched the government money market fund Franklin OnChain US Government Money Fund (FOBXX) on the Stellar chain. FOBXX is the first U.S.-registered mutual fund to use a public chain for transaction processing and recording share ownership. It is regulated by the U.S. Investment Company Act of 1940. From its registration, management and disclosure, this product is a market-leading One of the most compliant RWA products on the market. FOBXX is currently the largest product on the RWA U.S. debt track.

According to the FOBXX official website, it invests more than 99% of its total assets in securities fully mortgaged by the U.S. government, and its assets have excellent creditworthiness. The share of the FOBXX fund is represented by the BENJI token. The BENJI price is stable at US$1. It is mainly for American investors, and both institutional and retail users can participate. FOBXX distributes the income from U.S. Treasury bonds to BENJI holders through the application it developed, Benji Investments App.

At present, FOBXXs total assets exceed US$300 million, with an annualized rate of return (APY) of approximately 5.28%. From the perspective of institutional strength, product scale, start-up time, compliance, etc., Franklin Templeton is the well-deserved leader of the RWA U.S. debt track.

(2)Mountain Protocol

Mountain Protocol is an income stable currency protocol. Its main business is to issue stable currency USDM with U.S. Treasury bonds as collateral, allowing users to enjoy the income from U.S. Treasury bonds while using USDM.

USDM is issued by Mountain Protocol Limited, and its collateral is short-term US Treasury bonds. The company has obtained a digital asset business license from the Bermuda Monetary Authority (BMA) to ensure its compliance. Users mint/exchange USDM stablecoins with 1 USD and use them in various DeFi ecosystems. The Mountain Protocol adjusts the total supply of USDM based on the yield of U.S. Treasury bonds, so that the USDM balance held by users increases accordingly.

Using Mountain Protocol requires KYC certification, and due to the need to comply with relevant laws, the protocol does not provide services to domestic users in the United States, and currently only opens casting and redemption channels to institutional investors, and retail users can only purchase in the secondary market.

The current total asset size of USDM is approximately US$150 million, with an annualized rate of return (APY) of approximately 5%. As an interest-bearing stablecoin, Mountain Protocols USDM currently mainly challenges the status of traditional stablecoins such as USDT and USDC, but in essence, as a RWA asset, it also has great development potential.

(3)Matrixdock

Matrixdock is a digital asset platform owned by Matrixport, and its development goal is to provide RWA tokenization solutions. The product currently launched by Matrixdock is STBT, which is a token guaranteed by U.S. Treasury bonds and a reverse repurchase agreement collateralized by U.S. Treasury bonds as the underlying asset.

Similar to USDM, the interest-earning method of STBT is that the project party distributes it to STBT holders every day based on the rate of return of the underlying assets, increasing the amount of STBT held in their accounts. Unlike USDM, USDMs on-chain transactions do not require permission, but Matrixdock restricts STBT through the contract whitelist mechanism to only be able to be transferred and traded between accounts authorized by Matrixdock. In addition, STBT is minted using USDC or USDT, which is more in line with the usage habits of users on the chain.

In addition, the issuance of STBT also adopted the method of establishing a special purpose company to achieve complete bankruptcy protection (not affected by Matrixport). Matrixdock also uses Chainlink’s Proof of Reserve (PoR) to increase the transparency of STBT.

STBTs current total assets are approximately US$95 million, with an annualized rate of return (APY) of 5.10%. Matrixdocks official website has also reserved display positions for other types of RWA assets, but details have not been announced yet. As the RWA U.S. bond issuer currently ranked 4th in TVL, if Matrixdock wants to overtake others in a corner and introduce more novel underlying assets to the chain, it may have a chance to win.

3. Project roadmap

Ondo’s roadmap for the next two years consists of three main phases:

Phase One: Focus on integrating tokenized cash equivalents such as USDY, OUSG and OMMF. This includes establishing partnerships with different blockchains, adding white-label tokens for brand equity on other chains, and creating different token versions for different applications (author’s note : It can be simply understood as developing tokens according to specific standards, customizing them to a certain extent according to the requirements of the project party, and selling them as OEM, similar to the concept of sheathing).

Innovative technologies such as Ondo Bridge and Ondo Converter are designed to facilitate cross-chain transfer and conversion of tokens, integrating these tools to provide a seamless user experience.

The second stage: focus on expanding the tokenization of public securities. Ondo is preparing to announce initiatives to redefine the tokenization of public securities, addressing the major barriers that currently limit the widespread use of tokenized securities on public blockchains, such as liquidity and infrastructure issues (Author’s Note: Stocks, companies that can be traded on the open market Financial derivatives such as bonds, REITS and even options and futures all fall under the category of public securities).

Phase 3 (specific details have not yet been disclosed): Explore the application of blockchain in a variety of traditional financial functions, while leveraging centralized and decentralized mechanisms to maintain Ondo’s institutional-grade quality standards.

During these phases, Ondo will work closely with partners, including various blockchains, OTC desks, market makers, exchanges and DeFi protocols to ensure broad distribution, integration and liquidity of the product.

4. Project safety

Ondos smart contracts have been audited by many well-known industry institutions, including:

January 2023 Code 4 rena audit

NetherMind Audit April 2023

August 2023 Zokyo Audit

September 2023 Code 4 rena audit

4. Ondo Finance Token Economy

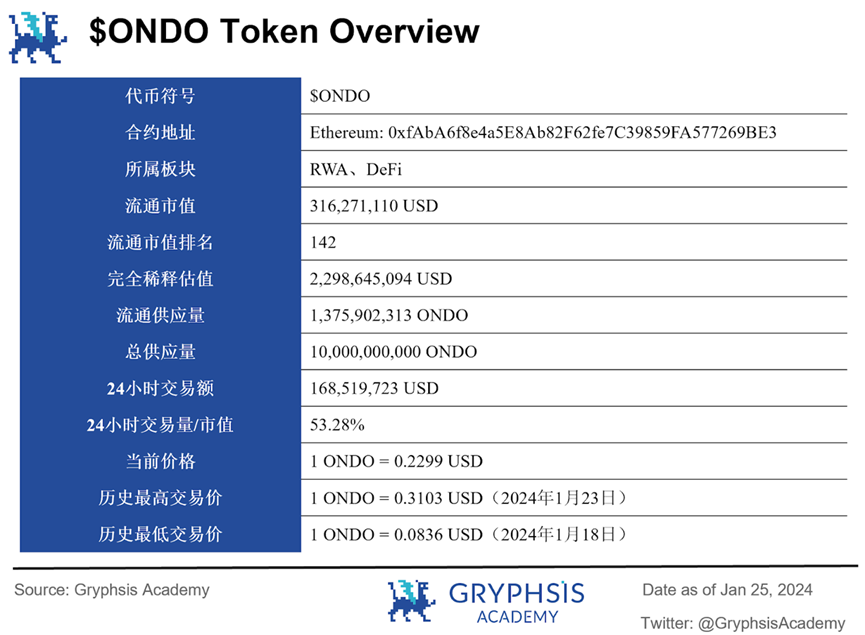

1. Basic information of Ondo Finance tokens

As of January 25, 2024, the basic information of the $ONDO token is as follows:

2. Actual use cases of Ondo Finance tokens

As of now, $ONDO is the governance token of Ondo DAO and has no other practical use cases. There are no incentives for $ONDO tokens to use Ondo Finance related products.

According to Ondo Foundation:

Ondo DAO grants $ONDO holders the following specific rights related to Flux Finance, which rights are currently governed by Ondo DAO:

Launch of new fToken market (i.e. supporting new assets as collateral and/or loanable within the Flux protocol)

Suspending fToken market

Update interest rate models for each market

Update oracle address

Withdraw fToken Market Reserves

Ondo DAO has the following additional rights:

Select new administrator

Manage asset library

Control the release of $ONDO to effectively increase the usage of Ondo DAO products

Call any function

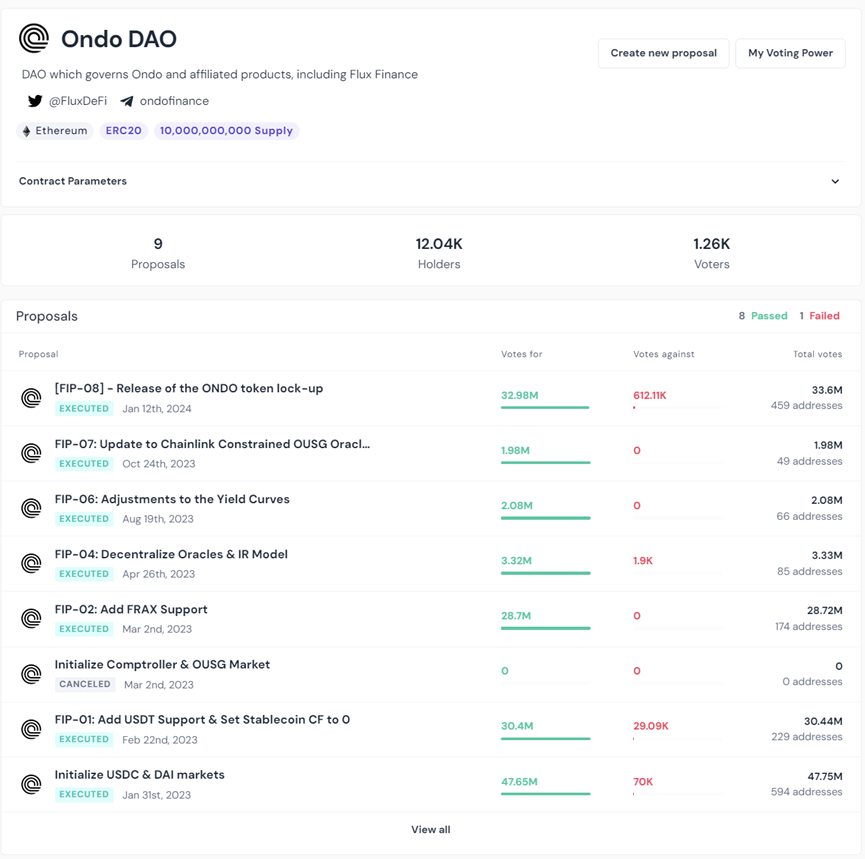

As of January 25, 2024, a total of 9 proposals were launched on Ondo DAO, of which 8 were passed and 1 was canceled.

Since it is not yet clear how the $ONDO token is related to RWA products, the market speculates that Ondo may use $ONDO as an incentive for tokenized financial products such as USDY in the future.

If $ONDO tokens can be combined with RWA products and use $ONDO tokens as an incentive to flow on the RWA product chain, it may push RWA products into the eyes of public crypto investors.

3. Ondo Finance Token Distribution

According to the Ondo Foundation’s proposal on December 27, 2023, $Ondo is planned to be distributed as follows:

Community Sales: 198, 884, 411 (~2.0%)

Ecological growth: 5, 210, 869, 545 (~52.1%)

Protocol Development: 3,300,000 (33.0%)

Private Placement Sales: 1,290,246,044 (~12.9%)

As of now, nearly 80% of $Ondo tokens are still stored in the project wallet and have not yet been distributed.

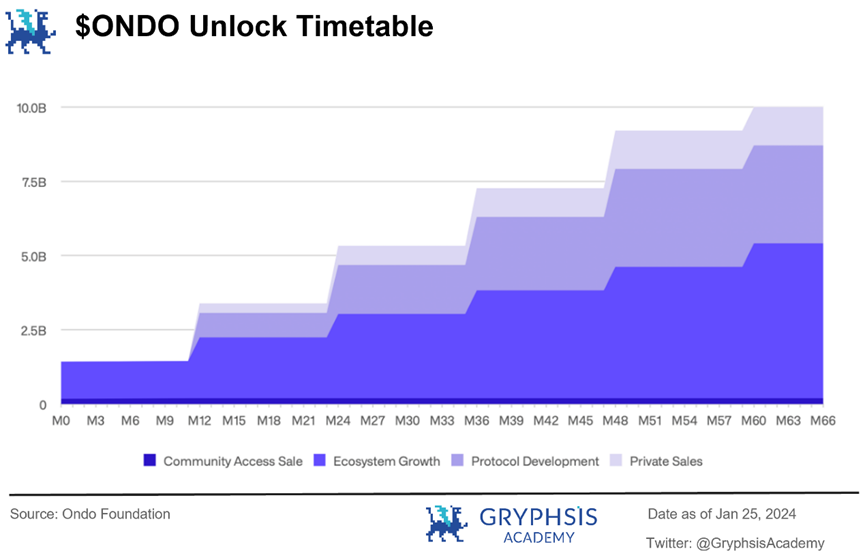

4. Ondo Finance token unlocking schedule

According to the Ondo Foundations proposal, more than 85% of $ONDO tokens will be locked, and the locked tokens will be unlocked 12, 24, 36, 48 and 60 months after the initial token unlock. Both private equity investors and project teams will be locked in for at least 12 months and will be unlocked in the next 4 years. Investors who participated in the ICO through CoinList have all been unlocked on January 18, 2024.

It is worth mentioning that in the past few days, the Ondo projects address has transferred $ONDO tokens to the exchange address many times (the current $ONDO in the projects wallet is less than 80% of the total circulation). It may be that the project Party lends tokens for market making.

5. Ondo Finance token price trend

Community investors’ $ONDO was unlocked on January 18, 2024, and has been trading in the secondary market for only 7 days. Its historical trend is as follows:

In addition, the primary market trading price of $ONDO before unlocking is as follows:

Seed round financing in August 2021:

1 ONDO = 0.0057 USD

Series A financing in April 2022:

1 ONDO = 0.0285 USD

May 2022 ICO financing:

1 ONDO = 0.055 USD

6. Main trading place for Ondo Finance tokens

According to data from CoinMarketCap, the main trading venues of $ONDO are Bybit, HTX and Gate.io. The specific distribution is as follows:

7. Ondo Finance other on-chain data

5. Ondo Finance project analysis conclusion and risk warning

To sum up, the main highlights of Ondo Finance are as follows:

The RWA U.S. debt track where Ondo Finance is located has experienced a 6-fold increase in TVL in the past year. It is the main driving force of the RWA industry and the industry prospects are very bright.

Ondo Finance ranks third in the TVL of the RWA U.S. Debt Track, where it has proven the feasibility of its business model and has a certain first-mover advantage.

Ondo Finance is already planning RWA products for other types of assets. If it can first launch products that are easily accepted by the market in the future, it will further expand its leading advantage and become an important bridge connecting the on-chain and off-chain.

Ondo Finance cooperates with leading companies in the industry such as Morgan Stanley and Coinbase (Coinbase is also an investor in Ondo) and strictly abides by relevant US laws and regulations, making it easier to gain the trust of investors.

The founders and core team of Ondo Finance have worked for Goldman Sachs, Morgan Stanley, Tether, Bitfinex, Circle and other companies, which is conducive to further in-depth cooperation with the above-mentioned companies.

The main risks of Ondo Finance are as follows:

The RWA track has just started, and many leading and powerful institutions are also vying to enter this field. Ondo Finance will face very fierce market competition in the future.

In addition to being the governance token of Ondo DAO, the $ONDO token has no other practical use cases. Ondo Finances related products are not strongly associated with $ONDO. The future usage scenarios of $ONDO are questionable.

About 80% of $ONDO tokens are still in the hands of project parties, the distribution mechanism is still unclear, and there is a large risk of centralization.

References

1. Ondo Finance Docs

2. Unlocking ONDO: A Proposal from the Ondo Foundation

https://blog.ondo.foundation/unlocking-ondo-a-proposal-from-the-ondo-foundation/

3. CoinList-Ondo

4. Former Goldman Sachs employees launch DeFi protocol Ondo with $ 4 million in seed funding

5. Peter Thiel's Founders Fund co-leads $ 20 million Series A for Ondo Finance

https://www.theblock.co/post/143769/ondo-finance-raises-funding-peter-thiel-founders-fund

6. Ondo Finance Overview

https://www.reflexivityresearch.com/paid-reports/ondo-finance-overview

7. Asset Risk Assessment: Ondo and Flux Finance (OUSG)

[Statement] This report is produced by@longyeyouxin, a student at @GryphsisAcademy, in@CryptoScott_ETHand@Zou_BlockOriginal works completed under the guidance of. The authors are solely responsible for all content, which does not necessarily reflect the views of Gryphsis Academy, nor the views of the organization that commissioned the report. Editorial content and decisions are not influenced by readers. Please be aware that the author may own the cryptocurrencies mentioned in this report. This document is for informational purposes only and should not be relied upon for investment decisions. It is strongly recommended that you conduct your own research and consult with an unbiased financial, tax or legal advisor before making any investment decisions. Remember, the past performance of any asset does not guarantee future returns