Original author: Matrixport analyst Markus Thielen

Original compilation: Wu Shuo

Summary

In the first half of 2024, the crypto industry will have five micro events and one macro event that may have a positive impact on the industry and potentially push the price of Bitcoin higher.

By January 2024, we expect the SEC to approve a Bitcoin ETF, with trading expected to begin in February or March.

Stablecoin issuer Circle may list on the stock market in April.

While news of FTX’s winning bid may be announced in December 2023, we expect the exchange to be operational by May or June 2024. FTX is expected to regain its position as a top 3 exchange within 12 months.

The above three events and the Bitcoin halving cycle are expected to provide healthy momentum in the coming year.

Although it is challenging to consider it a significant upside catalyst, Ethereum’s EIP-4844 upgrade is scheduled for Q1 2024.

This is also consistent with a potential Fed rate cut in mid-2024, as markets are pricing in a first rate cut in June 2024.

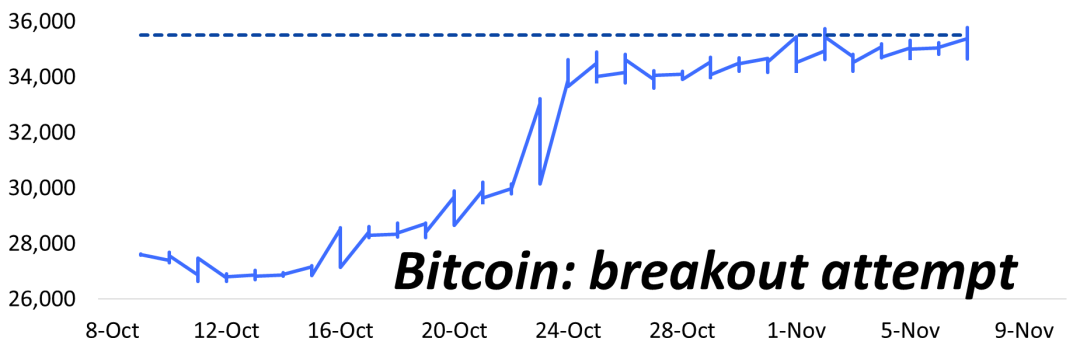

If inflation falls again, next weeks U.S. CPI data could spark another rally for Bitcoin. We expect Bitcoin to attempt to break out of its recent trading range of $34,000 to $35,000. A break above $36,000 could push Bitcoin towards the next technical resistance at $40,000, possibly reaching $45,000 by the end of 2023. With a steady increase in buyers during U.S. trading hours, and continued attempts at a Bitcoin breakout, we could see prices rebound towards the end of the month (and year-end). The Santa Claus quote can start at any time.

Chart 1: Bitcoin is trying to break higher – aiming for $40,000, maybe even $45,000

Expected potential impact of U.S.-listed Bitcoin ETFs in 2024

In the first half of 2024, the crypto industry will have five micro events and one macro event that may have a positive impact on the industry and potentially push the price of Bitcoin higher. Cryptoassets had a strong year in 2023, outperforming most other assets. Our fundamental value proposition is a U.S.-listed Bitcoin ETF with Registered Investment Adviser (RIA) potential, managing $5 trillion in assets primarily through ETFs, using Bitcoin as the cornerstone of a multi-asset portfolio. An allocation of just 1% would result in $50 billion in Bitcoin inflows.

Chart 2: Year-to-date performance of select assets

By January 2024, we expect the SEC to approve a Bitcoin ETF, with trading expected to begin in February or March. Stablecoin issuer Circle may list on the stock market in April. While news of FTX’s winning bid may be announced in December 2023, we expect the exchange to be operational by May or June 2024. The above three events and the Bitcoin halving cycle are expected to provide healthy momentum in the coming year. Although it is challenging to view it as a significant upside catalyst, in the first quarter of 2024, Ethereum’s IEP-4844 upgrade is scheduled to take place. At the same time, the U.S. Federal Reserve may cut interest rates in mid-2024, as the market is pricing in a first rate cut in June 2024. This occurs when macro liquidity shifts from tailwinds driven by peak interest rates to doubling liquidity through rate cuts.

Our year-end price target moves from ambitious to achievable

A year ago, we published a report titled “Bitcoin Could Rally to $63,160 in March 2024.” In the report, we believe that ideal Bitcoin buying opportunities historically occur 14-16 months before the next halving, in late October 2022, when Bitcoin is trading around $20,000. However, it was our report published on December 2, 2022, “Bitcoin Could Reach $29,000 in 2023, Driven by Macroeconomics”, that based our predictions that U.S. inflation will decline and provide massive amounts of money for the crypto market. In anticipation of liquidity, the report expects Bitcoin to rise by 70%.

Inflation has indeed declined significantly since then, and while cryptocurrency fundamentals such as Ethereum revenue data have been weak, the upward momentum in the cryptocurrency market is likely to reaccelerate as we enter 2024. A month ago, the market entered another inflection point, which may provide enough momentum for the continuation of the fifth bull market. When we published our report, the year-end 2023 target of $45,000 we set on February 3, 2023, appeared ambitious given that Bitcoin was trading at $22,500 at the time. However, with prices moving higher towards the $40,000 level, this price target may be achievable.

Unleashing the potential of institutional investors

Chart 3: Grayscale GBTC’s discount to NAV has narrowed from -45% to -14%, outperforming Bitcoin

Grayscale’s Bitcoin Trust (GBTC) stock appears to be held by 61 institutional firms — in addition to other investors such as high-net-worth individuals, family offices, and others — anyone with reportable assets below $100 million. The SPDR Gold (GLD) ETF has 1,090 institutional investors and is similar to BlackRocks iShares Gold ETF. The BlackRock Bitcoin ETF alone can attract more than 1,000 institutional investors. While approximately 45 million Americans already hold cryptocurrency, 160 million Americans have stock investments. The potential impact investors have on the cryptocurrency market remains huge but often underestimated. This influx could significantly increase liquidity in the cryptocurrency market and greatly improve fiat-to-crypto pipelines, which are currently mostly limited to Tether — at least based on the real-time data we can monitor.

Spillover: Coinbase IPO and FTX’s new owner

In anticipation of Coinbase’s initial public offering (or direct listing) on April 14, 2021, Bitcoin price has surged to $61,500. There is a concerted effort by all parties to create as much hype as possible. Market commentator Jim Cramer tweeted that we are bullish on Coinbase at $475, giving the company a similar valuation to Goldman Sachs. Although the company gave a reference price of $250 per share, many (mainly) retail investors believed they could buy shares at that level, valuing the company at $65 billion. IPOs tend to bring huge momentum to an industry as media coverage intensifies, and Coinbase attracted the most customers during the pre-IPO stage.

The stock opened at $381, peaked at $429.5, and closed at $328 on its first trading day. Today, the stock trades at $88, 77% below its direct listing price, and has a market capitalization of $21 billion. Coinbase has approximately 98 million users, and 9 million people trade on Coinbase every month.

Chart 4: Claims as a percentage of creditor value - FTX claims tripled this year

When FTX collapsed a year ago, Coinbase had a market capitalization of $12 billion. In its last funding round, FTX was valued at $32 billion and is said to have 8 million registered users, including 5 million active users. Despite the scandal and recent conviction of Sam Bankman-Fried, the FTX brand and its user base continue to have significant value. By December 2023, new owners may take over the exchange. We believe FTX could be sold for $2-3 billion, an attractive price considering the number of registered users and its global brand recognition. The customer churn is mainly attributed to SBFs inner circle, while the exchanges brand value is relatively intact.

Matrix on Target expects the little-known cryptocurrency exchange “Bullish” to acquire the entity. Well-funded through Block.one ownership and well-connected with deep-pocketed investors, Bullishs exchange desperately lacked an active user base (and was in desperate need of a better name, after Matrix on Target humble opinion)). FTXs price tag will likely continue to benefit FTX creditors. FTX creditor claims were trading above 55 cents by some estimates, and that was before there was clear news of the exchange being sold to another investor. SEC Chairman Gensler also said that FTX may be relaunched under new leadership. This suggests that cryptocurrencies are here to stay and that the SEC has not explicitly excluded cryptocurrencies. The new owner will likely use significant marketing resources and offer incentive fees to retain users of the exchange. This will create huge momentum that will benefit the overall sentiment in the cryptocurrency market.

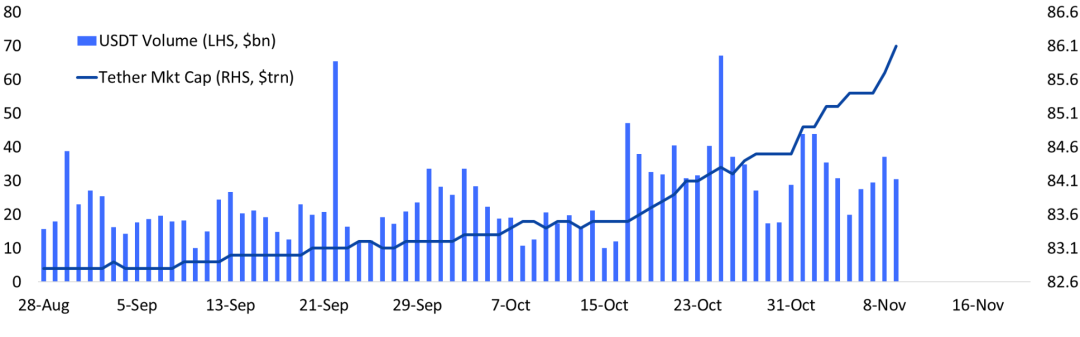

Circle’s IPO ambitions and Tether’s stunning market capitalization growth

Stablecoin issuer Circle is also expected to restart its IPO plan. In late 2022, a SPAC (special purpose acquisition company) deal that aimed to value the company at $9 billion failed. This shows that crypto operators are increasingly confident that the crypto bull run will continue into 2024, if not longer. However, critical investors may point out that Coinbases IPO occurred at a time when the market was near the absolute top, leaving many investors sitting and waiting to take their losses.

Over the past 12 months, Circle’s USDC market capitalization has dropped by -47%, from $45 billion to $24 billion. Much of the decline occurred in March 2023 when the U.S. government seized three important banks for cryptocurrency investors. Circle itself is in trouble, as at least one of the three banks has billions of dollars sitting there. But despite (or because of) Circle’s regular audit details and close cooperation with U.S. regulators, investors prefer Circle’s bigger brother, USDT.

Chart 5: TetherUSDT market value rises sharply, new minting means new inflow, $86 billion

While the market value of USDC has declined last year, Tethers USDT has grown by 30%, from $66 billion to $86 billion, reaching an all-time high. Even in the last month, it seems that another $3 billion has flowed into the crypto market as the market capitalization continues to increase. Since mid-October 2023, these flows have risen again as investors become increasingly convinced that the macro environment is favorable for cryptocurrency liquidity conditions.

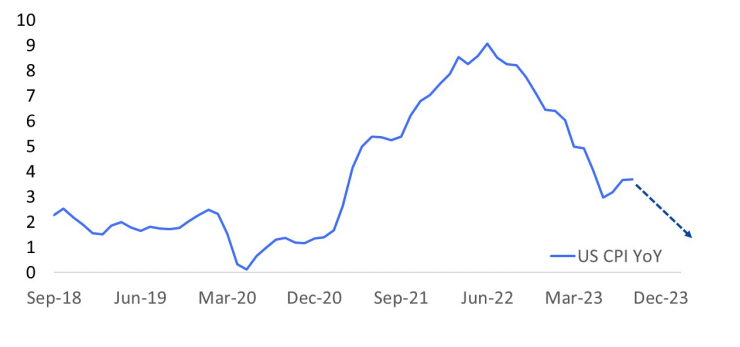

As macro data signals strengthen, Bitcoin is about to break through the impact of inflation and macro factors on Bitcoin trading behavior.

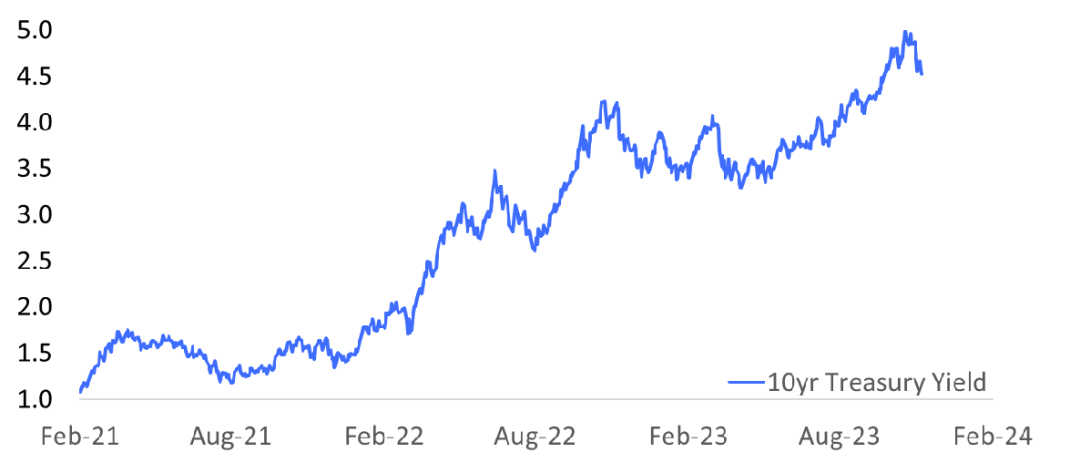

Two months ago, US inflation (CPI) unexpectedly rose from 3.2% to 3.7%. This rise breaks the ongoing decline in inflation, which may explain why Bitcoin was trading relatively calmly between $25,000 and $26,000 in late summer.

As our readers know, declining inflation has been a huge driver of macro liquidity since November 2022 and is a key reason why Bitcoin prices have surged more than 113% this year. A month ago, U.S. inflation was stuck at 3.7%. Bitcoin prices rose from $27,000 to $34,000 a week after the inflation data was released, as traders grew more comfortable with this level and viewed it as a temporary increase.

Chart 6: Along with inflation, U.S. Treasury yields have been a headwind for cryptocurrencies in 2022

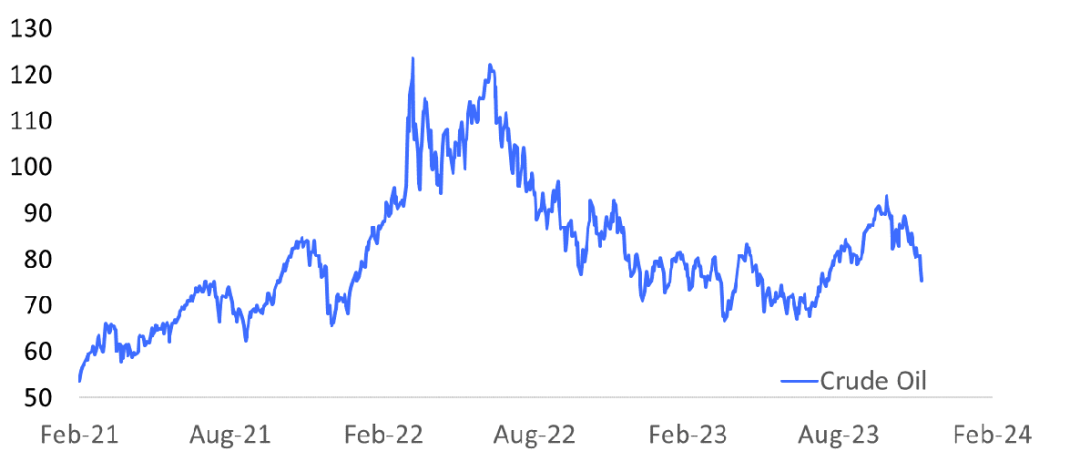

Other factors may also have played a role, such as the short-term gamma of Bitcoin options market makers or positive statistics related to the “unfortunate” Friday the 13th Bitcoin purchase. However, as we have demonstrated many times, falling inflation data triggered a rise in Bitcoin prices earlier this year. Crude oil prices are up more than 30% from summer lows, which could affect inflation expectations. Still, oil prices have fallen -20% since late September. Traders may expect inflation to fall again, which supports risk assets from a macro liquidity perspective.

Chart 7: Falling oil prices could trigger another round of lower U.S. inflation

If inflation falls again, next weeks U.S. CPI data could spark another rally for Bitcoin. Ahead of the release of this data, we could see Bitcoin attempting to break out of the recent $34,000-$35,000 trading range. A break above $36,000 could push Bitcoin towards the next technical resistance at $40,000, possibly reaching $45,000 by the end of 2023.

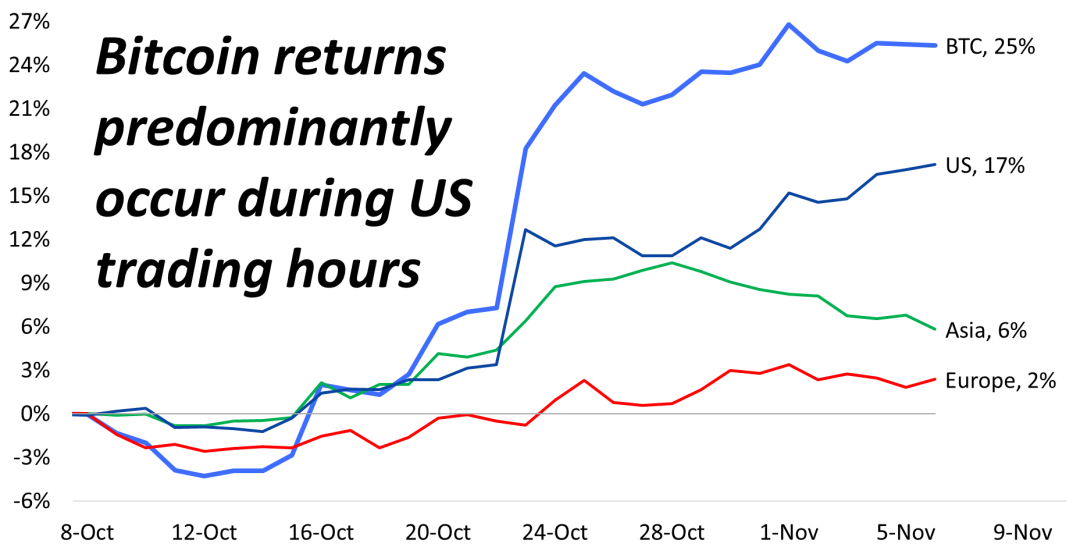

Trading Patterns: US Bitcoin Buying Activity Steady

Chart 8: Bitcoin price surges mainly during U.S. trading hours

Notably, despite Bitcoin’s decline during the Asian trading session, it saw sustained and gradual buying activity during the U.S. trading session. One possible explanation is that Asian traders favor altcoins over Bitcoin.

However, while Ethereum’s returns increased by +16%, it is worth noting that 70% of these returns (equivalent to +11%) occurred during the US trading session. Solana, on the other hand, maintains a more balanced performance in all three regions. This is surprising as flows from Europe are relatively small compared to volumes during US and Asian trading sessions. The even distribution of traffic can be attributed to the Solana Breakout Conference in Europe (Amsterdam).

Three macro-positive data emerged last week: 1) The U.S. Treasury Department slowed the pace of long-term bond issuance, suggesting bond yields should fall; 2) Chairman Powells dovishness at the post-FOMC press conference stance, indicating that the Fed is unlikely to raise interest rates again during the cycle; 3) U.S. employment data is disappointing, reinforcing the first two points.

Chart 9: Slight rise in CPI over summer keeps Bitcoin range-bound

The next key macro data point will be US CPI (inflation) data, due out next Tuesday (November 14). With a steady increase in buyers during the U.S. trading session and Bitcoin’s continued attempts to break out, we may see prices rebound towards the end of the month (and into the year). The Santa Claus quote can start at any time.