Original author: TechFlow

The once hot encrypted payment card (U card) business is now facing shrinkage.

On June 17, Infini co-founder Christine posted on X, announcing the cessation of consumer-oriented encrypted U card business, and also elaborated on the reasons behind it:

Compliance costs are high, margins are thin, and operational burdens are heavy.

She admitted that the to C card business took up 99% of the company's time and costs, but brought almost no revenue contribution. This announcement also marks Infini's strategic withdrawal from the to C card business and its focus on financial management and B-side services.

But 1-2 years ago, U Card was seen as a breakthrough innovation combining cryptocurrency with traditional finance.

By supporting direct consumption of stablecoins such as USDT and USDC, U Card quickly attracted users in the crypto circle; at that time, ChatGPT had just emerged, and many people wanted to experience the subscription service, but due to the lack of overseas bank card payments, U Card also became a new payment channel in this AI craze.

Withdrawals and ChatGPT, the former represents the crypto community’s desire for channel security, while the latter activates new payment scenarios.

From the current perspective, with the development of the industry, these two demands do not seem to have a rigid demand for U cards. As more U card projects fail one after another, the difficulty of this business becomes more and more obvious.

Not an isolated case

Infini's exit is not an isolated incident.

We can obtain from public information that there are many examples of partial or complete closure of U card business, the more typical ones are:

In September 2024, OneKey announced that it would stop new registration and recharge functions, and officially stop using its U card service on January 31, 2025. Although the official did not elaborate on the reason, the industry speculated that it was related to the interruption of upstream payment service providers or compliance pressure;

In December 2023, Binance terminated its card services in the European Economic Area, and ended cooperation in Latin America and parts of the Middle East in August 2023. This adjustment is considered a response to stricter regional regulations;

Back in 2018, Visa, one of the world's largest payment networks, terminated its cooperation with WaveCrest due to compliance issues. The latter is an intermediary that provides card issuance and payment processing for crypto payment cards and is responsible for connecting U cards to the Visa network. Visa's sudden withdrawal directly resulted in WaveCrest being unable to continue serving its customers, including U card providers such as Bitwala and Cryptopay.

These cases all point to one fact: the U card business is facing systemic difficulties worldwide.

Upstream out of control and high costs

From the perspective of ordinary users, the U card is a very simple product - what you see is what you get, and you can use it as soon as you get it; the only things that need to be weighed and compared are the rates and wear and tear.

But from the perspective of U card manufacturing, the root of the problem lies in its complex upstream and downstream logic and high cost pressure.

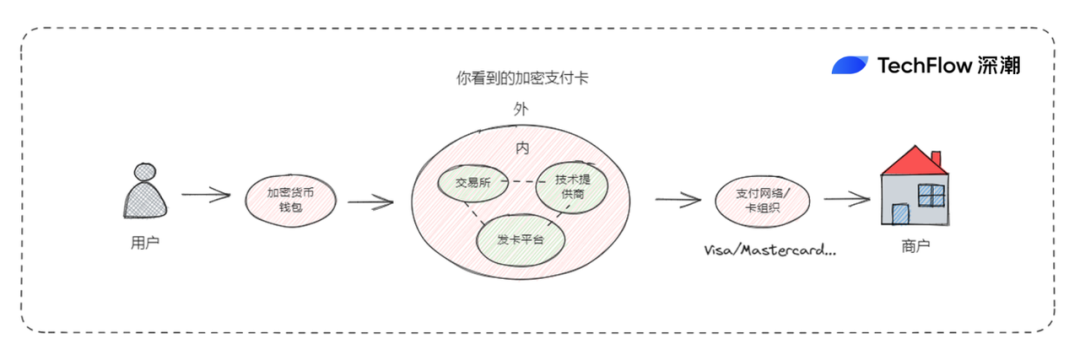

First of all, the operation of U Card relies on the collaboration of multiple parties: users recharge stablecoins such as USDT, card providers (such as Infini) convert cash into fiat currency through off-ramp withdrawals, and payment networks (such as Visa, Mastercard) complete settlement with card issuers and banks.

However, the upstream links, especially payment networks and banks, are not under the control of the crypto community. This makes U Card a "vassal" of the traditional financial system with weak bargaining power.

But why do you see so many different brands of USB cards?

Exchanges are issuing cards, wallets are issuing cards, and payment startup teams are also issuing cards... Can anyone issue a crypto payment card?

When users see a card with a cryptocurrency exchange brand and a VISA logo, what is unknown behind it is actually the cooperation model between the card issuer and the technology provider.

For example, Coinbase’s VISA card was previously supported by technology provider Marqeta, which enables it to issue crypto debit cards and provide users with real-time transaction authorization and fund conversion services;

Furthermore, due to the existence of the role of "technology provider", the issuance process of crypto payment cards becomes relatively simple.

Technology providers offer a capability similar to "Card Issuance as a Service": by providing organizations that need to issue cards with the necessary security technology, payment processing systems, and user interfaces to support crypto card issuance, currency conversion, and payment.

Card issuers only need to call the technology provider's API or SaaS solution to issue and manage encrypted credit/debit cards.

At the same time, the technology provider's "Card Issuance as a Service" also includes a variety of functions including transaction authorization, funds conversion, transaction monitoring and risk management, helping issuers simplify operations and improve efficiency.

(For a clearer explanation, please refer to the previous article: " The Business behind Crypto Payment Cards: The Rush to Issue Cards ")

In other words, the U card in your hand is actually the result of cooperation among multiple parties including the card issuer, technology provider, bank and payment network.

At the same time, this also means that everyone in the card issuance chain has a profit-making appeal. Everyone wants to get a piece of the pie, while the card issuance projects and brands that are relatively downstream in the entire chain can obviously not get much benefit from it.

U Card's revenue mainly comes from transaction fees, but the 1-3% fees charged by the payment network, the additional costs of stablecoin conversion, and bank account maintenance fees will quickly eat up the profits of this business.

Revenue is difficult to cover costs, but what is more troublesome is that fixed costs cannot be cut.

Supporting the operation of U Card is not an easy task. Technical maintenance needs to process transactions in real time and ensure security, while customer support needs to deal with refunds and consultation needs. For example, the 10-working-day refund arrangement promised by Infini requires human support and response.

On the user side, individuals may encounter problems due to various payment scenarios, but the project parties of the U card business must deal with these personalized issues; and because the upstream chain is too long, when problems arise with the technology provider or card organization, resulting in service suspension/abnormality, they are often caught in the crossfire.

Compliance Risk

In addition, the survival of U Card also faces strict compliance requirements. KYC and AML (anti-money laundering) are the basic thresholds, and if doing business in North America and Europe, the US FinCEN registration and EU MiCA regulations are further added.

USDT itself is also one of the favorite assets of gray industries (such as money laundering and money laundering), which naturally determines that U Card needs to spend more energy to deal with risk control issues.

Even more radical is that when a U card business company operates in the mode of "registered overseas, with employees working in China", due to the particularity of the encryption industry in China, this business is more likely to face certain legal risks.

Recently, there have been reports on social media that some U card businesses have been shut down. We cannot know the authenticity and specific details of the incident itself, but one thing is certain:

The efforts that the U card business needs to make in complying with local regulations, as well as the risks brought about by other factors, are much higher than those of many businesses on the chain. Sometimes it is not necessarily a problem with the card itself. The funds involved in the card, the people who use it, and the relatively tight public opinion environment may all cast a shadow on the brand and perception of the U card business.

It's a thankless job and no money is made from worrying. This may be the common dilemma faced by most U card projects in the payment field.

The current U card business may be more suitable for CEX. CEX does not rely on U cards to generate profits and income. When the trading business can generate sufficient profits, it is a better choice to manage customer loyalty through U cards and treat it as a brand differentiation service.

For example, Bybit and Bitget still have corresponding U cards, and Coinbase recently stated at the State of Crypto Summit that it will launch Coinbase One Card in the fall of 2025. Users can get up to 4% of Bitcoin back for each transaction, and the card is supported by the American Express network.

Everyone wants to issue the card, but who can finally do it is more of a test of compliance resources and risk control capabilities. From the current situation, the U card business is gradually becoming an oligopoly.

From vassalage to independence

On the one hand, cryptocurrencies are hindered from doing traditional business, while on the other hand, it has become a trend for traditional finance to continue to do business related to the cryptocurrency circle.

Whether it is stablecoins, RWA or the recently popular encrypted asset reserves of US-listed companies, traditional finance is profiting from "stealing" in the cryptocurrency circle by relying on existing resources and compliance accumulation;

As for the cryptocurrency business, apart from the crypto-native businesses centered around transactions and on-chain asset creation, the cryptocurrency industry is increasingly feeling controlled by others as it tries to expand outward.

The dilemma of the U card business actually reflects the awkward situation of the entire crypto industry when interacting with the traditional financial system. As a "vassal" of traditional finance, the crypto industry has never been able to take the initiative in the payment field.

Perhaps reducing dependence on fiat currency conversion, initiating transactions directly from wallets, conducting transactions directly through on-chain settlement, and bypassing traditional payment networks to transfer money are the original forms of encryption technology. However, under the premise of compliance and embracing reality, this path seems too idealistic.

If, however, the traditional business is controlled by others and the company attempts to control the industry chain, such as acquiring banks, payment channels and technology providers, this will probably further increase the cost of the business, especially when it is not known how many users will use the card.

Going further, if we look at the contradictions reflected in the U card business, we will find that they are not only in the payment field, but also throughout the extended development of the entire crypto industry.

When innovation and enthusiasm can only continue in the native soil of crypto, the opportunity for grassroots, independent crypto to break out of the circle has still not arrived.