The US payment giant PayPal announced last night that it will launch a compliant digital stablecoin called PYUSD. The stablecoin will be issued by Paxos Trust (the former issuer of BUSD) and will be fully backed by deposits in US dollars, short-term government bonds, and similar cash equivalents. It will gradually be made available to PayPal customers in the US over the next few weeks. Eligible US customers will be able to buy and sell PYUSD directly through PayPal at a price of $1.

In addition to supporting transfers of PYUSD between PayPal and compatible external wallets, it also supports exchanges with any other cryptocurrencies. Furthermore, PayPal provides users with available payment scenarios, including the option to use PYUSD for purchases and person-to-person payments.

In the future, PYUSD will also be supported by the mobile payment service Venmo. Considering that Venmo processes nearly $10 billion in transactions per month and PayPal currently has 430 million users, it is imaginable the massive adoption that will occur when retailers start accepting PYUSD as a form of payment.

Compliant on-ramps and off-ramps are expected to bring more liquidity into the crypto ecosystem. The payment scenarios built around real use cases establish a connection between stablecoins and traditional finance and the real economy. These are positive market signals for the crypto bear market.

While the traditional financial system is moving towards digital currencies, native crypto projects are also striving to bridge the gap to the real world and actively seek their own real users. They include "crypto debit cards that can be used to buy coffee," "peer-to-peer self-hosted payment systems," "crypto-native wallets," and "international fiat off-ramp services for enterprise users."

Regardless of their specific implementation, they all have one common feature, which is "bringing on-chain and off-chain together." This enables the crypto industry to intersect with the real world, offering another possibility beyond RWA (real-world assets).

Low-cost, compliant, crypto-native, non-custodial wallets that are as smooth to use as WeChat Pay are helping the crypto industry embrace more real users. Perhaps we can start with everyday activities like buying coffee with cryptocurrency.

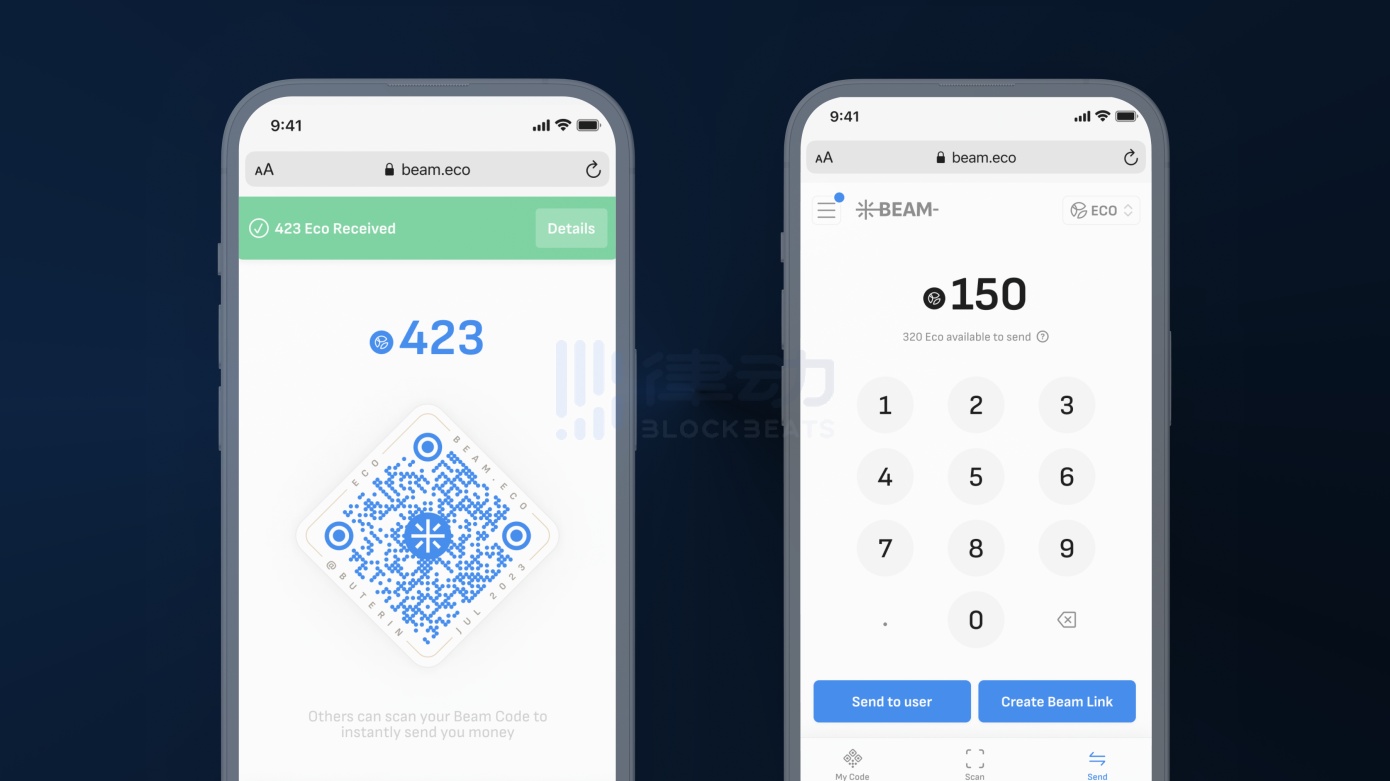

Non-custodial P2P Payment System Beam

Beam is a self-hosted payment wallet that supports stablecoins and ECO tokens. It has a user-friendly interface similar to Web2 P2P applications and offers a smooth user experience. It supports peer-to-peer payments and aims to become the on-chain version of Venmo.

The key advantage of Beam is that it not only provides a smooth native encryption payment experience, but also reduces the payment cost to a negligible level.

Native encryption means that the wallet is non-custodial, and centralized entities such as banks or exchanges cannot access users' funds. However, currently, non-custodial wallets face the challenge of "complex user experience". Beam's goal is to make decentralized wallets intuitive enough that even people who have just encountered cryptocurrency can get started in minutes.

By adopting the ERC-4337 account abstraction standard, Beam removes a series of complex concepts such as wallet addresses, blockchains, keys, mnemonic phrases, and ETH gas fees. Even novices who have never dealt with cryptocurrencies can use cryptocurrencies for remittances without any worries. Newcomers can create a wallet by visiting the official website, and then associate their Twitter account to save wallet login and access permissions.

In addition, Beam supports users to pay transaction fees with tokens. For example, if you transfer USDC, you can pay the transfer fee with USDC (no need for ETH). By adopting the Optimism and Base networks, Beam's transaction fees are also low enough.

In the early stages, Beam targets peer-to-peer payment scenarios and aims to build a global version of Venmo on the blockchain, especially in dollar-denominated areas outside the United States. The ultimate goal is to become a global version of Visa.

This application is "immediately available globally", in contrast to traditional financial products that "need to be launched country by country because you have to touch the banking rails of each country."

Beam is launched by Eco, a crypto payment startup supported by a16z. Eco has raised a total of $95 million in funding, with other investors including Coinbase Ventures, Founders Fund, Lightspeed Venture Partners, and Pantera Capital.

Gnosis Card: A Visa debit card tied to wallets

Gnosis Card is an encrypted debit card issued by Gnosis, which is directly linked to the user's on-chain account. It supports users to use digital assets in their wallets to make purchases in any store that accepts Visa cards, in order to meet the needs of Web3 users to pay for daily goods with stablecoins. The goal is to achieve the use of cryptocurrencies as if they were fiat currencies.

Although the adoption in the offline physical world may still be far away, ordinary users can also achieve freedom of cryptocurrency consumption in the real world through the real-time conversion of fiat currencies to physical assets.

Underlying Technology Network: Gnosis Pay

Gnosis Card is supported by Gnosis Pay, a decentralized payment network developed by Gnosis itself. It is based on Polygon's zkEVM and acts as a Layer 2 chain. It supports any Layer 1 network that is EVM compatible, and can achieve faster and cheaper transactions compared to Layer 1 chains.

Whether it's the offline banking system, Visa, MasterCard, Alipay, etc., they can directly interact with this Layer 2 payment network, and users' Safe contract payment wallets run on this Layer 2.

It is worth noting that as one of the important partners of Gnosis Card, the Euro stablecoin EURe issued by Monerium will be used by Gnosis Pay for on-chain and off-chain payments to reduce bridging risks. At the same time, Monerium supports users to associate their crypto wallets with international bank accounts or IBANs, and correspondingly, each Gnosis Card will be associated with a Safe wallet account.

When users remit from their bank accounts to the IBAN associated with the wallet, EURe stablecoins will be automatically minted on Ethereum and blockchains like Gnosis, and will be displayed in the wallet. Conversely, when users spend from their wallets, the stablecoin EURe will be burned, and the corresponding Euro will be sent to the user's bank account.

Although there are complex operations behind it, connecting the world of "on-chain" and "off-chain", "fiat currency" and "physical entities", involving layer one and layer two settlement payments, for consumer users, the experience is as smooth and convenient as traditional credit card and WeChat payments. According to the [team's demonstration at EthCC](https://twitter.com/levi0214/status/1680936353138343941), a transfer transaction can be completed in about one to two seconds, and the gas fee cost is less than $0.1.

How to solve DeFi compliance issues?

Non-custodial does not mean non-compliant or in violation of any existing regulations. On the contrary, adopting compliant methods to achieve decentralized financial payments is becoming a trend, which means that DeFi is moving in the right direction, which is a positive development for the entire industry.

Fractal provides KYC process-related services support for Gnosis Pay. Specifically, when users apply for Gnosis Card using a Monerium bank account, Fractal's system allows users to share verified identities with Gnosis through on-chain message signing.

The focus of compliance is to comply with data privacy regulations. This requires developing a solution that allows data to be distributed between "private but unpermissioned node alliances (meaning no entity can control the blockchain)". Unlike the InterPlanetary File System (IPFS) for distributed file storage, this requires Fractal to "ensure data coverage in order to comply with the right to be forgotten."

The right to be forgotten, also known as the right to deletion, is a key provision of the General Data Protection Regulation (GDPR). It grants individuals the right to request organizations to delete their personal data and requires organizations to comply with these requests within a specified timeframe.

In other words, the solution provided by Fractal allows users to control their own data and provide access to designated entities within a specified timeframe in accordance with legal requirements. As the obligor entities are subject to financial regulatory scrutiny, financial regulatory agencies may require them to provide information about the parties behind the IBAN number.

In addition, Gnosis Pay will also collaborate with partners to screen for fraudulent activities.

Each user has a Safe account on the Gnosis layer one chain and a corresponding account on zkEVM (a layer two Ethereum scaling solution built on Polygon), similar to savings and spending accounts.

Gnosis Pay's compliance partners will conduct anti-money laundering (AML) and countering the financing of terrorism (CFT) screenings on the funds entering the L2 account. This means that all funds entering L2 are screened and can be spent immediately via the Visa network. Users have full control over the two Safe accounts and can transfer back to L1 at any time. In other words, the role of L2 is to ensure compliance and enable the network to process a large number of payments, which is the fundamental purpose of the L2 solution.

Integration with Existing Financial Systems

Gnosis Pay provides users with a seamless native cryptocurrency payment experience. However, behind the scenes, there is a series of complex processes. In reality, Gnosis Pay needs to integrate with existing financial systems to facilitate transactions, such as becoming a member of Visa and Mastercard.

It is worth noting that as one of the important partners of Gnosis Card, the Euro stablecoin EURe issued by Monerium will be used by Gnosis Pay for on-chain and off-chain payments to reduce bridging risks. At the same time, Monerium supports users in associating their cryptocurrency wallets with international bank accounts or IBANs. Once the wallet address is associated, users will receive an IBAN account that can be used to "send and receive euros in the SEPA system (including CEX)".

As the world's first Web3 IBAN, Monerium is an authorized and regulated electronic money institution (EMI). Its authorized and regulated Web3 euro token "EURe" can be used on Ethereum, Polygon, and Gnosis, and supports the sending and receiving of euros between any bank account and Web3 wallets (Metamask, Safe, and Argent).

IBAN is a standardized system widely used in Europe to identify cross-border bank accounts. When users remit funds from a bank account to an IBAN associated with a wallet on blockchains such as Ethereum and Gnosis, EURe stablecoins are automatically minted and displayed in the wallet. Conversely, when users spend from the wallet, the stablecoin EURe is destroyed, and the corresponding euros are sent to the user's bank account.

Holyheld: Web3 Debit Card

Holyheld is a Web3 debit card supported by Polygon's zkEVM. Registering on the official website (http://holyheld.com) will give you an encrypted payment card with an International Bank Account Number (IBAN). It provides cryptocurrency-to-fiat exchange services and cryptocurrency wallet services, supporting stablecoin USDC and most mainstream cryptocurrency wallets. Android and iOS apps will be launched in the future, but physical cards have not been released yet.

Holyheld can connect to multiple non-custodial wallets, including Argent, Coinbase Wallet, MetaMask, and Rainbow. It supports multiple networks such as Arbitrum, Gnosis Chain, Optimism, and Polygon without the need for bridging and centralized compromise.

Holyheld supports users to access http://holyheld.com or the app to order cards, and the virtual cards will be immediately available. Users can also add them to Google Pay (Apple Pay will be launched soon) and start using Holyheld without the physical card.

Virtual Credit Card OneKey Card

OneKey Card is a virtual VISA card service launched by the globally well-known digital hardware wallet OneKey. It supports users to pay for daily expenses with cryptocurrency. Users can recharge in the form of USDT/USDC and use it online and offline on major domestic and international e-commerce platforms. OneKey Card is a prepaid card that supports mainland ID verification and can be bound to electronic payment platforms such as Alipay, WeChat Pay, and PayPay for consumption. It supports most domestic consumption scenarios.

OneKey Card supported consumption scenarios include: overseas shopping (supporting consumption on platforms such as Amazon, Walmart, eBay, Shopee, Lazada, etc.), currency conversion (convert cryptocurrencies into USD, HKD, etc.), software subscriptions (used for deducting fees for services like OpenAI / ChatGPT Plus API), daily expenses (can be bound to Meituan for payment of delivery, dining, travel, and other services).

However, starting from September 30th, OneKey Card will no longer accept new user applications from mainland China, Russia, and other regions. On August 8th, hardware wallet OneKey announced that starting from September 30, 2023, OneKey Card will stop accepting new user applications from the following countries or regions: Iran, North Korea, Syria, Russia, North Macedonia, mainland China, Sudan, Venezuela, and Zimbabwe. Users who have already activated the card will not be affected and can continue to use it normally. This move is to strictly comply with local laws and regulatory requirements, and to support more scenarios in the future such as Apple Pay. Physical cards are also included in the plan.

Utopia Labs: USDC Withdrawal Service for Enterprise Users

Utopia Labs, previously focused on becoming a DAO payroll payment system, has recently transformed into a transfer service for USDC stablecoins for enterprise users, aiming to accelerate the adoption of cryptocurrency payments.

This product supports enterprise entities worldwide in sending USDC to US bank accounts, bridging the gap between fiat currency and cryptocurrencies, and improving the speed and convenience of transactions by avoiding centralized exchanges.

This is especially useful for companies that receive salaries and fundraising in cryptocurrencies, such as using USDC to pay service providers with US bank accounts, such as office rent. Other potential use cases include venture capital funds paying investments to project parties or cashing out on-chain revenue from crypto projects.

How to Apply?

Enterprise users can submit KYB and KYC verification applications to Utopia Labs and wait for approval within 2 working days. Once approved, enterprise users can exchange USDC for USD at a 1:1 exchange rate, and Utopia Labs will charge a 0.3% fee. USDC transfers are unique to the Ethereum blockchain and have no restrictions, and they comply with ACH (Automated Clearing House) transfers, typically received within three working days.

Utopia's roadmap includes withdrawal services for any token (not just USDC) and will support other blockchain networks in the future, as well as provide fiat deposit services. This service is available in most countries/regions except for Cuba, North Korea, Iran, Syria, Belarus, and Russia. In addition to crypto payments, Utopia Labs also offers treasury management for Safe (formerly known as Gnosis Safe) users, providing token swapping services through integration with the 0x protocol and liquidity across over 100 decentralized exchanges.

Prior to this, Utopia Labs focused on building a DAO payroll system and raised a $23 million Series A funding round in 2022, led by Paradigm with participation from Circle Ventures and Coinbase Ventures, valuing the company at $115 million.

Trends and Key Insights

Although these products have different implementation methods, we can identify some common trends and key insights in the realm of non-custodial payment consumer products:

1) Account abstraction provides a seamless user experience, allowing users to use cryptocurrency like traditional credit cards.

Without exception, these products prioritize user experience. Despite being native to crypto and non-custodial wallets, they offer a smooth experience similar to traditional payment tools. This is mainly achieved through the application of the ERC-4337 account abstraction standard, abstracting the complexity behind the underlying technology and removing concepts such as wallet addresses, blockchains, keys, mnemonics, and ETH gas fees. This allows even novice users to use cryptocurrency for payments and transfers without any concerns.

2) Additionally, as mentioned by David Hoffman from Bankless in his experience at ETHCC, "underlying performance optimizations are ready, waiting for the bull market and users." The optimization and improvement of these underlying solutions will significantly reduce payment costs.

3) Non-custodial wallets mean that central entities, such as banks or exchanges, cannot access users' funds. This is becoming an increasingly attractive practical demand for consumers, especially after the FTX incident. Non-custodial does not mean non-compliance; on the contrary, it must be compliant and move in the right direction. This is also a trend we observe. Fractal offers KYC identity verification services to ensure compliance with data privacy laws. In addition, Gnosis Pay's partners conduct anti-money laundering (AML) and counter the financing of terrorism (CFT) screenings on funds entering L2 accounts. For Gnosis Pay, the L2 solution built on Polygon zkEVM not only facilitates low-cost processing of a large number of payments but also ensures final compliance.

4) The freely combinable underlying technology stack is equivalent to developing products on the shoulders of giants.

One of the advantages brought by blockchain technology is "permissionless openness and composability," which means that most of the time, creating an application does not require starting from scratch, but rather making the best use of the existing foundational building blocks.

This is a typical characteristic of most Web3 products. Lens Protocol, a Web3 social graph protocol, is a representative example. It has formed a thriving ecosystem based on multiple technology stacks. These stacks are compatible with each other, freely combinable, and can utilize existing components developed by others, while also being open to being used by others. This approach can greatly improve productivity.

As a type of consumer product, non-custodial wallets are no exception. In order to reduce transaction fees, they generally use layer-two scaling solutions. To optimize user experience, they also need to adhere to account abstraction standards and provide important standardized compliance services for decentralized finance.

For example, Gnosis Pay, its founder shared the underlying technology stack of Gnosis Pay, including: Safe for implementing account abstraction, Gelato for gasless transactions, Polygon zkEVM for layer-two chain development, and Monerium for providing solutions for deposits and withdrawals.

ethcc shows us the situation of "underlying performance optimization is ready, waiting for users to come." As blockchain infrastructure gradually matures and improves, and various protocol layers and middleware emerge, this way of developing products, which is akin to standing on the shoulders of giants, may change the current scarcity of consumer products.

5) Integration with existing financial systems.

Behind the smooth native cryptocurrency payment experience are a series of complex processes, including integration with traditional financial systems such as Visa and Mastercard.

In addition, regulated electronic money institutions (EMIs) like Monerium also serve as a bridge. As the world's first Web3 IBAN, once users associate their wallet addresses with Monerium, they can obtain an IBAN account that can be used to "send and receive euros in the SEPA system (including CEX)". It supports the use of authorized and regulated Web3 euro tokens "EURe" issued by Monerium on Ethereum, Polygon, and Gnosis, as well as sending and receiving euros between any bank account and Web3 wallets (Metamask, Safe, and Argent).

Reference source:

https://www.theblockbeats.info/flash/159950?search=1

https://twitter.com/andy_bromberg/status/1684605161308925952

https://echo.mirror.xyz/FbaqedtGg7SZuwOXesLnO8-Gk-Nzpna5ZvLZiw2TIFs

https://www.theblock.co/post/240880/paradigm-utopia-labs-usdc-bank-transfers