Original author: Grapefruit, ChainCatcher

Original author: Grapefruit, ChainCatcher

Since the beginning of February, the core developers of the Ethereum Foundation stated in a meeting that they will plan to complete the Shanghai upgrade in March, and the LSD (Lquid Staking Derivatives Liquid Staking Derivatives) track has become lively.

On March 15, the Ethereum Goerli testnet announced that it had completed the Shanghai upgrade. This Thursday, Ethereum developers will hold a meeting to determine the specific date for the mainnet upgrade. This Shanghai upgrade is also the first large-scale upgrade of Ethereum since it switched to the proof-of-stake mechanism (PoS) last September. This is of great significance to users, because the ETH 2.0 after the Shanghai upgrade will support users to retrieve the ETH pledged on the chain. After the deposit and withdrawal become more flexible, it will also inspire more users to pledge ETH to the chain.

As we all know, on the beacon chain, to become a verifier needs to pledge 32 ETH (or its multiples), and needs to bear the liquidity and opportunity cost of ETH while obtaining income. A certain technical threshold.

The birth of the LSD liquidity staking platform is to help users simplify the process of staking ETH while helping them obtain liquidity. Users only need to pledge ETH on the LSD platform, and it will replace users to participate in the pledge of the PoS mechanism to obtain income, and will also issue pledge certificate assets to users at a ratio of 1:1, releasing the liquidity of ETH during the pledge period.

Since the LSD platform provides ordinary users with the opportunity to participate in staking without maintaining the staking infrastructure and without thresholds, it has captured a large number of users and assets in a short period of time and developed into an independent track. As the Shanghai upgrade time approaches, the LSD track has naturally become a hot spot in the crypto market.

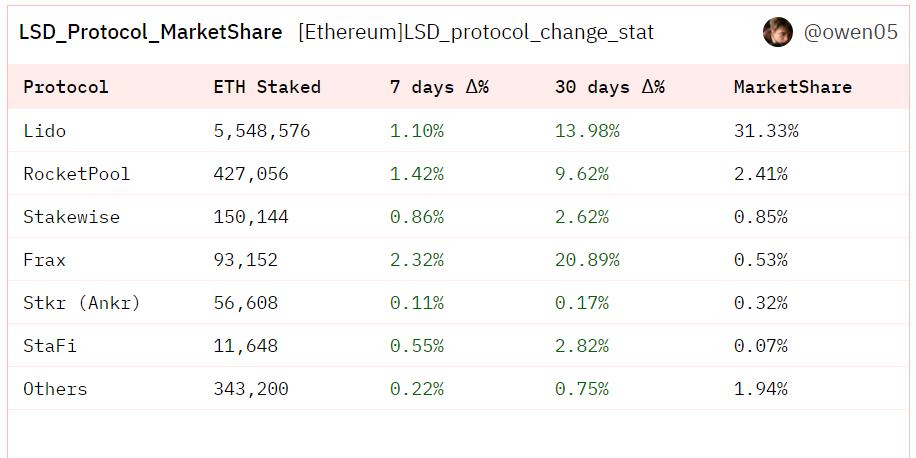

As of March 15, the Beacon Chain browser of Ethereum shows that there are currently about 549,000 active validators, and more than 17.579 million ETHs are pledged, worth about $29.8 billion, setting a record high. Among them, data shows that the market share of ETH pledged on LSD platforms such as Lido and Rocket Pool accounts for about 30%.

As an old-fashioned algorithmic stablecoin DeFi application, Frax has fallen into silence since the collapse of Terra's UST. Now, how does it regain user attention and occupy a place with the upsurge of LSD?

first level title

fxsETH has been live for 5 months, with more than $1.9 billion in pledged value

As of March 15, fxsETH has been online for less than 5 months, and its locked ETH has already reached 115,000, with a value of approximately US$1.932 billion.

fxsETH is an Ethereum liquidity staking product launched on October 21, 2022 by Frax, an old-fashioned algorithmic stablecoin application. It supports users to lock up ETH on its platform to obtain Ethereum 2.0 (ETH 2.0) block network pledge income and rewards.

According to the Dune data platform, the number of ETH pledged by fxsETH has increased by more than 20% in the past 30 days, and the market share of ETH pledged ranks fourth in the entire LSD track, second only to Lido, RocketPool, and Stakewise.

image description

LSD platform pledge related data, source Dune

Why can Frax attract so many ETH pledges in a short period of time? How is it different from the first liquid staking platforms such as Lido and Rocketpool?

How can Frax achieve higher returns when the block rewards of Ethereum 2.0 are relatively equal? This is due to the fact that Frax can adjust the two yields of "frxETH/ETH" and "sfrxETH" through the arbitrage mechanism. The former is the transaction fee income obtained by users using frxETH to form LPs, and the latter is to pledge frxETH again to obtain ETH 2.0 pledge income.

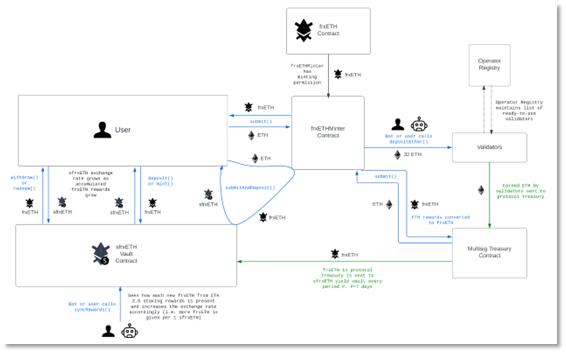

image description

frxETH official mortgage process

Specifically, Frax positions frxETH as “just a wrapper/synthetic asset pegged to ETH”, which users can obtain by minting (Mint) with ETH on the platform. However, the process of users using ETH to mint frxETH is irreversible, that is, users are not supported to exchange frxETH back to ETH on the official website, and holding frxETH has no income.

In previous staking platforms such as Lido and RocketPool, users pledged ETH to obtain pledge income. For example, Lido pledged ETH to obtain the certificate stETH for receiving the original assets and pledge income. However, users who hold frxETH need to operate again if they want to obtain benefits. There are two main ways:Staking to get Ethereum block network rewards:

First pledge ETH to frxETH, and then pledge frxETH to sfrxETH to obtain the pledge income of Ethereum 2.0. The annualized rate of return (APR) was about 7.8% in January. Today, the APR of sfrxETH has dropped to 6.49% ;Provide liquidity to obtain transaction fees:

First pledge ETH to frxETH, then provide liquidity for the frxETH/ETH fund pool on the Curve platform, and obtain transaction fees. The yield can reach more than 10% during the peak period. Currently, through the Convex platform, LP APR is about 5% .

During the same period, the return on ETH pledged by Lido was about 6%, and the return on ETH/stETH on Curve was about 6.43%.

It can be simply understood that, in fact, ETH pledge frxETH can get Ethereum 2.0 pledge rewards, but these rewards are only distributed to sfrxETH users who pledge frxETH again. frxETH users don’t get any rewards if they don’t pledge. If they want to get rewards, they either choose to pledge twice, or go to LP group to get rewards issued by Curve platform or Convex.

first level title

Seize LSD market share and control liquidity by adjusting yield

Theoretically speaking, whether the user chooses to use frxETH to form LP to provide liquidity for Curve's frxETH/ETH liquidity pool, or to pledge twice to become sfrxETH, mainly depends on the difference in the rate of return between the corresponding transaction fee income and pledge income .

How does this affect the Frax adjusted rate of return?

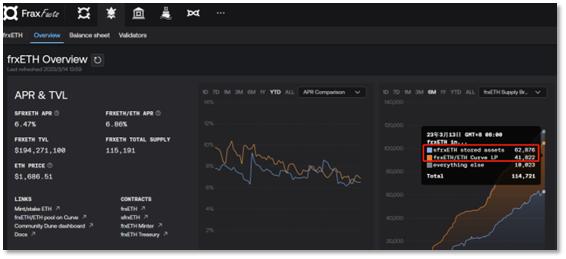

According to data from Frax’s official website, on March 15, Curve’s frxETH/ETH liquidity pool yield was 6.89%, and the second pledge sfrxETH was 6.49%. The yields of the two are relatively close, and the distribution ratio of frxETH between the two Also basically close.

image description

Distribution of frxETH in frxETH/ETH and sfrxETH

In fact, Frax can not only affect the balanced distribution of frxETH assets by controlling the relationship between the two yields of "ETH/frxETH LP yield" and "sfrxETH pledge yield". More importantly, Frax can also seize the LSD market share and control the liquidity of frxETH through this adjustment. For example, it can adjust the ETH pledge rate higher than the market level at any time, attract more users to pledge ETH, and control the depth and stability of the frxETH/ETH fund pool exchange through the LP rate of return.

How is Frax income regulation achieved? Frax holds the most Convex governance token CVX (approximately 20.5%), and Convex controls more than half of Curve voting rights (veCRV), which provides Frax with the weight to use CVX voting to influence the emission of capital pool rewards on Curve , so as to obtain the possibility of creating higher returns.

For example, Frax can affect the rate of return of Curve LP by regulating the bribery of Convex. For example, when the rate of return of sfrxETH is lower than the market average and wants to increase, Frax can increase bribery, so that the rate of return of Curve LP is significantly higher than that of sfrxETH pledged, which will attract more frxETH to choose to be Curve LP. The increase in the proportion of frxETH doing LP has brought about an increase in the sfrxETH pledge rate of return, and correspondingly, the depth of LP's increased capital pool has also increased.

Similarly, if the rate of return of Curve LP is lower than the staking rate of sfrxETH, frxETH/ETH LP may choose to withdraw liquidity, and more frxETH will choose to pledge again to become sfrxETH, so that the staking rate of sfrxETH will decrease until the second balance between them.

From this point of view, Frax is trying to find a differentiated competitive advantage for frxETH that is different from similar products such as stETH (Lido) through its influence and control over Curve's reward policy, allowing users to have a better arbitrage balance between frxETH and sfrxETH High yield options.

Today, with the launch of frxETH, Frax has finally successfully realized its influence on Curve again.

first level title

The second spring is ushered in doubts: Where is the business boundary of Frax?

Frax has attracted users to pledge ETH through the frxETH liquid staking product, which has also increased the value (TVL) of encrypted assets locked in the Frax application. According to DeFiLlama data, Frax's TVL is $1.34 billion, ranking 12th among all DeFi applications.

The new frxETH product seems to be giving this old DeFi application a second life.

However, some community users have questioned this: Frax has launched a series of products such as FPI (an anti-inflation stablecoin linked to CPI), loan Fraxlend, transaction Fraxswap and asset bridge Fraxferry since 2022. Why is it now online again? Pledge product frxETH? The team seems to be constantly developing new products, and the product line is very complicated. Where is its business boundary?

The person in charge of the Frax Chinese community answered this in an online live broadcast: Doing frxETH is a matter of course. We are optimistic about the growth of the LSD track in the future. frxETH will increase the asset management scale of Frax. The construction ideas and gameplay of frxETH products are similar Based on the stable currency FRAX, a new application scenario has also been built for the stable currency FRAX. He also revealed that Frax may build its own application chain in the future.

Some users also said: It is normal for DeFi applications to develop various products and try various businesses in the early stage, and DeFi applications should be allowed to try and make mistakes.

But Frax's most well-known and core business is still stable currency.

Launched in 2019 and created by a programmer named Sam Kazemian (Sam), Frax is the first algorithmic stablecoin application that adopts a hybrid mechanism. The economic model uses a dual-token mechanism of the stablecoin FRAX and the governance token FXS. The former is an algorithmic stablecoin that anchors the price of the US dollar, and the latter is a community governance token that can be used as part of the collateral assets for minting stablecoins.

The so-called mixed-algorithm stablecoin, that is, the stablecoin FRAX issued by Frax, is composed of part collateral (mostly USDC) and part algorithm mechanism (minting and burning of FXS). Frax’s original CR (mortgage rate) mechanism is similar to the central bank’s issuance of base currency, and is compared by users to the “on-chain Federal Reserve”.

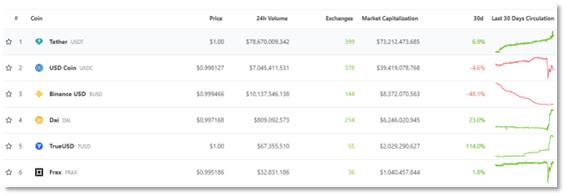

According to CoinGecko, FRAX currently has a market value of US$1.04 billion, making it the second largest stablecoin on the chain, followed by DAI with a market value of US$6.24 billion.

image description

FRAX's ranking on the stablecoin track

Frax was considered a stable head project when the Terra (UST) algorithm stable currency became popular in April last year, and the popularity of the two was indisputable. It is an important promoter of the Curve War war. It has also jointly tried to build the 4 pool (UST-FRAX-USDC-USDT) on Curve into the most stable cross-chain stable currency exchange pool with Terra, subverting the leading 3 pool (USDT- USDC-DAI), let UST and FRAX replace DAI. However, with the collapse of UST in May last year, the concept of Frax came to an abrupt end, and the interest in it also declined, entering a state of instability.

In February 2023, Frax announced that it would set the target collateralization ratio (CR) to 100%, remove the part supported by the algorithm, and make FRAX a fully collateralized stablecoin.

It wasn't until the LSD track was hot that the new product frxETH made this long-dormant old DeFi application stand in front of users again.

Frax still has a long way to go, though. For this hot new staking product, Frax is currently facing a series of doubts:

The reason why users choose to pledge ETH on Frax at this stage is because the income is higher than other LSD pledge platforms. The part that is higher than the staking income of ETH 2.0 can be seen as an additional subsidy given to users by Frax through the Convex and Curve platforms, but Convex’s high bribery has a cost. How long will this extra subsidy last? If there is no additional subsidy support, frxETH's income is the same as the current LSD platform, will users still choose it?