Original title: "Anatomy of the DCG Dumpster Fire"

Compilation of the original text: The Way of DeFi

Compilation of the original text: The Way of DeFi

The market is experiencing a slight uptick, but we're not going to lie, there's still a lot going on right now.

first level title

image description

Screenshot: Real Vision Finance

It's been a big week for Barry.

On January 2, Gemini co-founder Cameron Winklevoss posted an open letter to Digital Currency Group (DCG) CEO Barry Silbert on his Twitter, imploring Silbert to make a public commitment to repay with Gemini creditors before January 8. Debt of Genesis Global Capital reached agreement.

In a heartrending spiritual plea, Winklevoss offers a glimpse into the suffering of Gemini's retail savers: from the "father who lent his son money for his bar mitzvah" to the "single mother who lent money for his son's education." Becoming collateral to DCG’s “greedy share buybacks, illiquid venture capital investments, and kamikaze-style Grayscale NAV” have seen the (Grayscale) trust generate a massive surge in Assets Under Management (AUM).

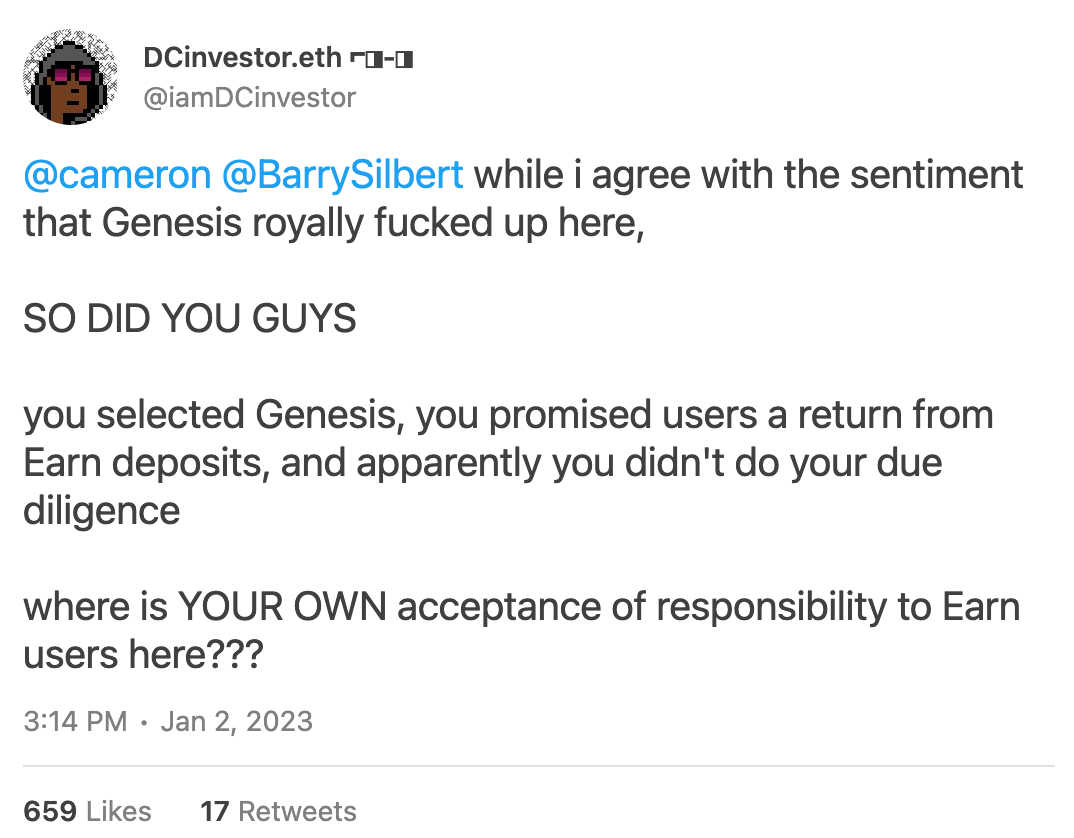

Genesis' largest creditor, Gemini, is owed $900 million. That's a good point, but Cameron, may I point out your apparent hypocrisy?

Encryption big V "DCinvestor.eth" replied to "Cameron Winklevoss" on Twitter, saying: "Although I agree with the point that Genesis screwed up here, so do you. You chose Genesis and promised users a return from Earn deposits , but clearly you failed to do your due diligence.”

image description

Source: Gemini

Having said that, at least the Winklevii family is trying to get better, DC!

While I'm by no means suggesting that the Winklevii should bear the financial burden of Genesis' missteps, or that Earn savers don't realize the risks they're taking, it does sound a bit like The pot calling the kettle black )...

first level title

debt

After Luna crashed back into orbit and 3AC went to hell, there was a big hole in Genesis' balance sheet. To keep its lending unit solvent, DCG assumed 3AC's debt and Genesis' role as a creditor.

With no liquidity, Genesis overcame insolvency through "accounting magic".

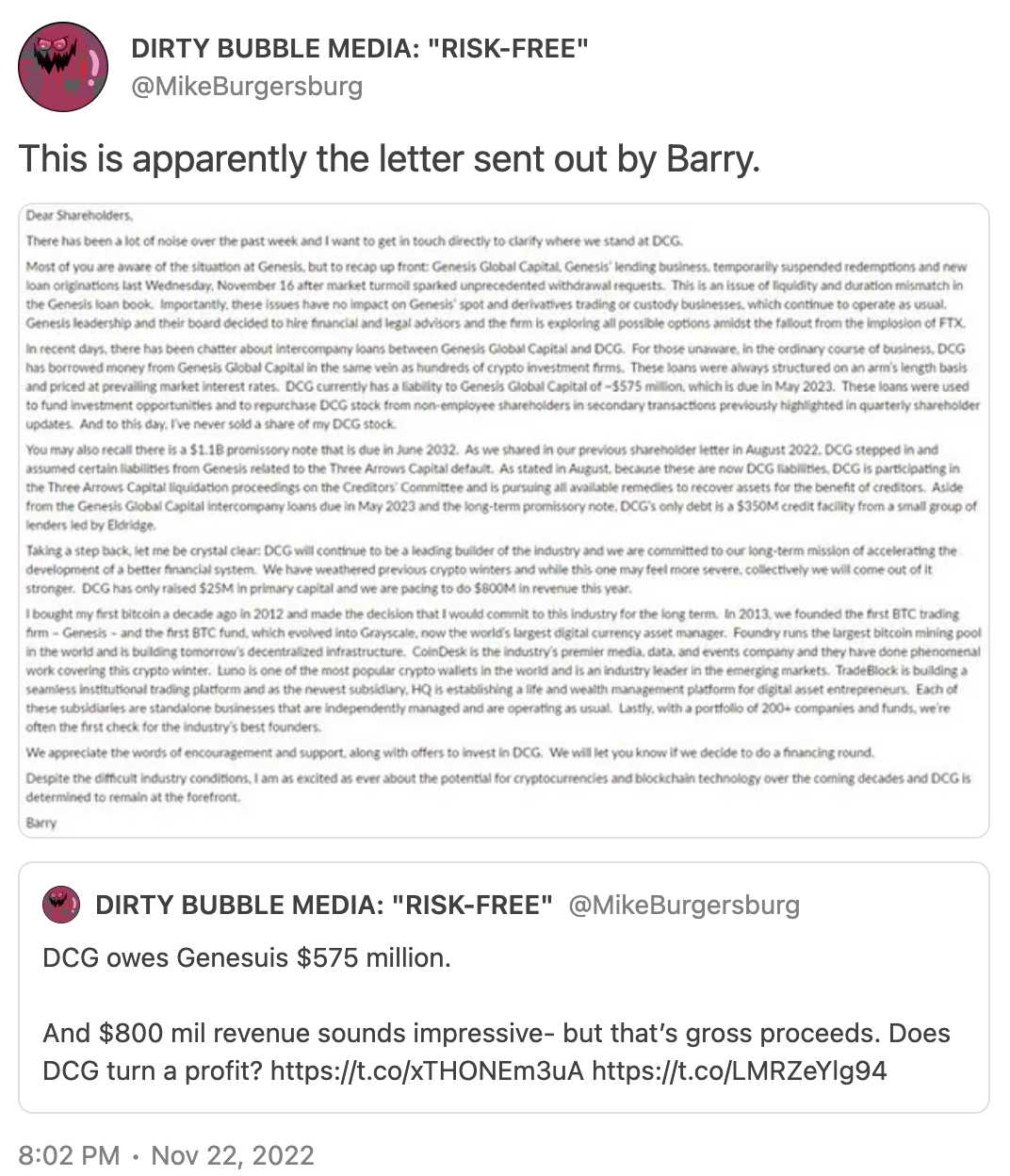

As 3AC fired on Genesis' balance sheet, DCG was forced to offer its subsidiary a $1.1 billion promissory note with a 10-year maturity. There is also an existing intercompany loan due in May for $575 million. In addition, DCG has a $350 million credit outstanding with Eldridge.

assets

assets

I'm sure astute Bankless readers may have deduced that it might be a challenge for DCG to find that gap to bridge in a bear market.

Grayscale, GBTC, and ETHE assets are currently the most liquid assets on DCG's books. Value can be extracted from these positions in two ways. Unfortunately for DCG, neither option generates enough cash.

Delphi Digital co-founder Tommy Shaughnessy tweeted: “DCG has two key choices here: 1. Sell Grayscale and sell GBTC/ETHE holdings – $600M + $471M = $1.071B; 2. Unwind Grayscale (if unsold it cannot be sold) and recover assets at par or $900m. We see either option as futile as it is ~1bn less than required $2.025bn Dollar."

The GBTC discount will be further increased if DCG chooses to pay a higher option, currently at 45.1%.

That leaves about $1 billion on DCG's venture capital book. Suffice it to say, the future of DCG looks grim.

Realistically, it would require a potential buyer to pay for the deal for it to make sense.

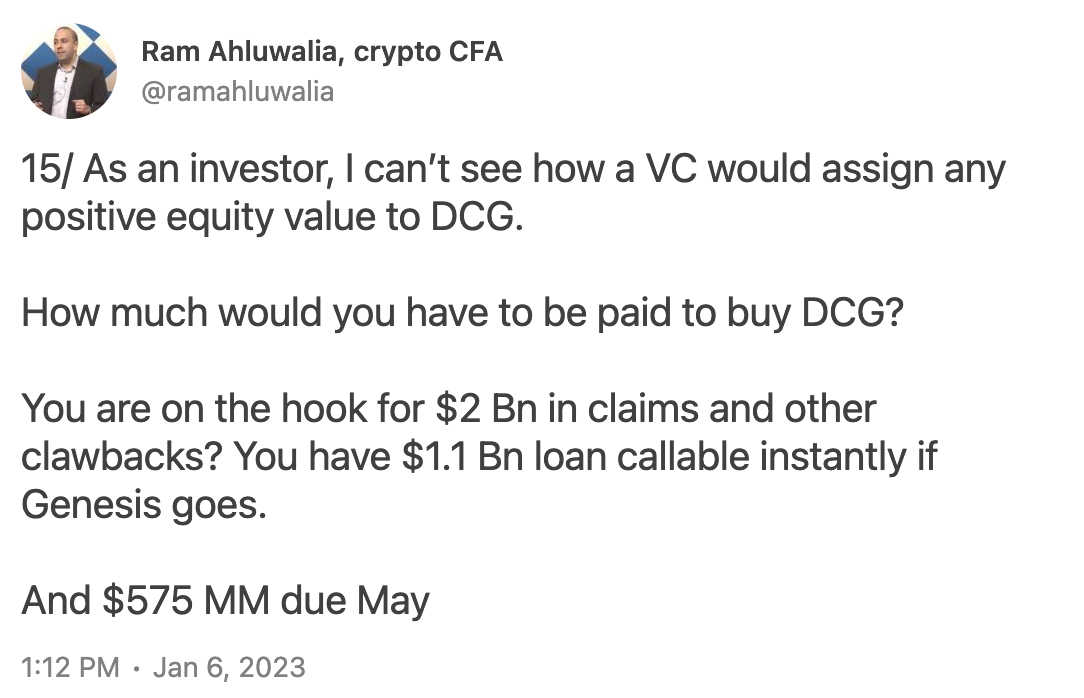

Ram Ahluwalia, CEO of Lumida Wealth, an encryption investment advisory firm, said, “As an investor, I don’t see how a venture capital firm (VC) would assign any positive equity value to DCG. How much do you need to pay to buy DCG? $2 billion in claims and other recovery costs? If Genesis goes bankrupt, you have $1.1 billion in loans immediately redeemable and $575 million due in May.”

first level title

question

secondary title

Monopoly Money is gone

As you've probably guessed in 2022, Digital Currency Group isn't doing much better in the new year.

After a disastrous year for the cryptocurrency space, it’s somewhat comforting to hear that the wallets of the wealthiest in the space have lost value along with the rest of us.

However, if one of your subsidiaries happens to be a cryptocurrency wealth management platform, you may not experience this joy.

Wealth management, like many financial industries, is a fee-based industry, which means the more assets under management (AUM) you have, the more money you can make.

Translate: It is easy to make money in a bull market, but difficult to make money in a bear market.

DCG has apparently learned that lesson, firing its WM division, HQ Digital, along with 60 employees in the company's latest round of layoffs.

Another salable asset and source of income disappears. Hello, sunk costs!

In the midst of the frantic cutbacks, any individual or group that becomes unprofitable due to changing market conditions will be put on the chopping block by DCG.

first level title

redeemable liabilities

key factor.

The once glorious DCG empire's best chance (extremely unlikely) has to wriggle out of the 2022 crypto crash.

The reason why Hal Press lost $10,000 in BTC.

Ironically, DCG may have shot itself in the foot in this regard, as it would dictate the terms of these intercompany notes!

Callable loans enable noteholders to demand repayment. Currently, DCG is indifferent to the callable note structure as it controls the behavior of the holder Genesis.

In bankruptcy proceedings, however, this will no longer be the case, and creditors of the estate may apply to the courts to recover their debts.

first level title

FBI?

Did you think Gensler (SEC Chairman) and Garland (US Attorney General) wouldn't surround the rotting corpse of a key crypto group like regulatory vultures? They also moved quietly late last Friday.

Investigators are "examining transfers between [DCG] and [Genesis]" in addition to "investors being told about the transactions," Bloomberg said.

The transaction in question could be:

a $575 million loan to DCG due May 2023; and/or a $1.1 billion promissory note due 2032.

Original link