Original source:Original source:

Blue Fox Notes

Ethereum Shanghai upgrade will generate a lot of selling pressure? Look at it from these 9 aspects

Many people are therefore worried, will there be a lot of selling pressure after the open pledge is unlocked? There are also bears who believe that the previous ETH USD price cost is low, and there will be good USD-based profits after unlocking, so the possibility of choosing to sell is also very high.

How to look at this problem?

According to the current situation, the high probability will not bring a lot of selling pressure (of course, future price changes will depend on more factors, and here we only discuss the single event of potential selling pressure). From nine perspectives:

1. Unlocking and withdrawal is released gradually, not flooding into the market all at once

At present, the mode of gradual unlocking is adopted. According to the current situation, theoretically, the upper limit of daily cash withdrawal is about 55,000 ETH. Ethereum can activate approximately 7.55 validators per epoch (total number of validators/65,536), 225 epochs per day. That is to say, about 55,000 ETH can be unlocked every day at most.

In addition, the withdrawal rate will be adjusted according to the total amount of pledged ETH to prevent instantaneous large outflows, etc.

2. Most of the users participating in the early pledge are long-term supporters of Ethereum

Those who are willing to take greater risks and uncertainties to enter the ETH pledge market in the early stage are all user groups with greater risk appetite. Most of them are relatively long-term and staunch supporters of Ethereum. These people are in the current bear market. Under the body, relatively speaking, the willingness to sell is small.

3. Many staking users who are willing to quit have already quit

Most of the staking participants use Lido or through CEX, and some have already exited. For example, users who pledge through the Lido protocol can convert their stETH into ETH through Curve, and can unlock it without waiting for Shanghai to upgrade. From the data point of view, there have been good discounts on stETH for several times last year. That is, some users who wanted to exit sold stETH for ETH. It also includes that due to the impact of some thunderstorms, some institutions have also withdrawn their stETH.

4. The openness of unlocking may be more attractive to institutions or large investors

With the opening of pledge unlocking, it is possible to attract more institutions or large investors to enter

First, this function itself brings confidence to more users;

Second, it can provide better exit channels for these users without worrying about exit liquidity or discount exit;

The third is that these users also need to obtain relatively stable income in the bear market (currently, the annualized income of the ETH currency standard can reach 4.2%, although it cannot be compared with DeFi in the bull market period, but in terms of the current market situation, for long-term supporters That said, the rate of return is still attractive).

Slap your head and estimate that after the opening of staking, there may be a slight decline in the short term, but the overall trend is upward, and it is possible to break through 20% of the total ETH in about a year.

5. The entry cost for ETH stakers is not low

According to the bearish cost theory, in fact, the average cost of entry is not low. The first batch of staked ETH costs around $500, but stakes are added incrementally. As a rough estimate (no precise data here), a large percentage of staking costs are roughly $1500+, which is higher than the current market price.

6. The asset nature of ETH has changed substantially after PoS

One is that ETH is currently gradually moving towards deflation, which has a huge impact on ETH.

After the ETH merger, it’s been 112 days so far, and since then, a total of 4,248 ETHs have been added (as of this writing). If there is no merger, then in these 112 days, 1,332,883 ETH will be newly issued, worth about 1.66 billion U.S. dollars, which means that the potential selling pressure will be reduced by about 15 million U.S. dollars per day. ETH holders can capture the value of its ecological growth even if it is in the wallet, does not participate in pledges, and does not participate in the income activities of the DeFI protocol.

The second is that ETH can obtain income through pledge.

At present, the annualized return is about 4.2%. When ETH has pledged income, ETH itself is not only the security supporter of the entire network, but also captures the income of its ecological growth, and ETH has fundamentally changed. As the ecology grows, it provides larger-scale security services for L2 and its network, and ETH will eventually benefit. That is, ETH has become the real underlying asset of the ecology. It is supported by more and more usage scenarios. When these networks reach a certain level, ETH will still have the opportunity to generate a currency premium. It is not only a payment medium within the ecosystem, but also gradually has the attribute of value storage. From this point alone, it is also competitive to BTC.

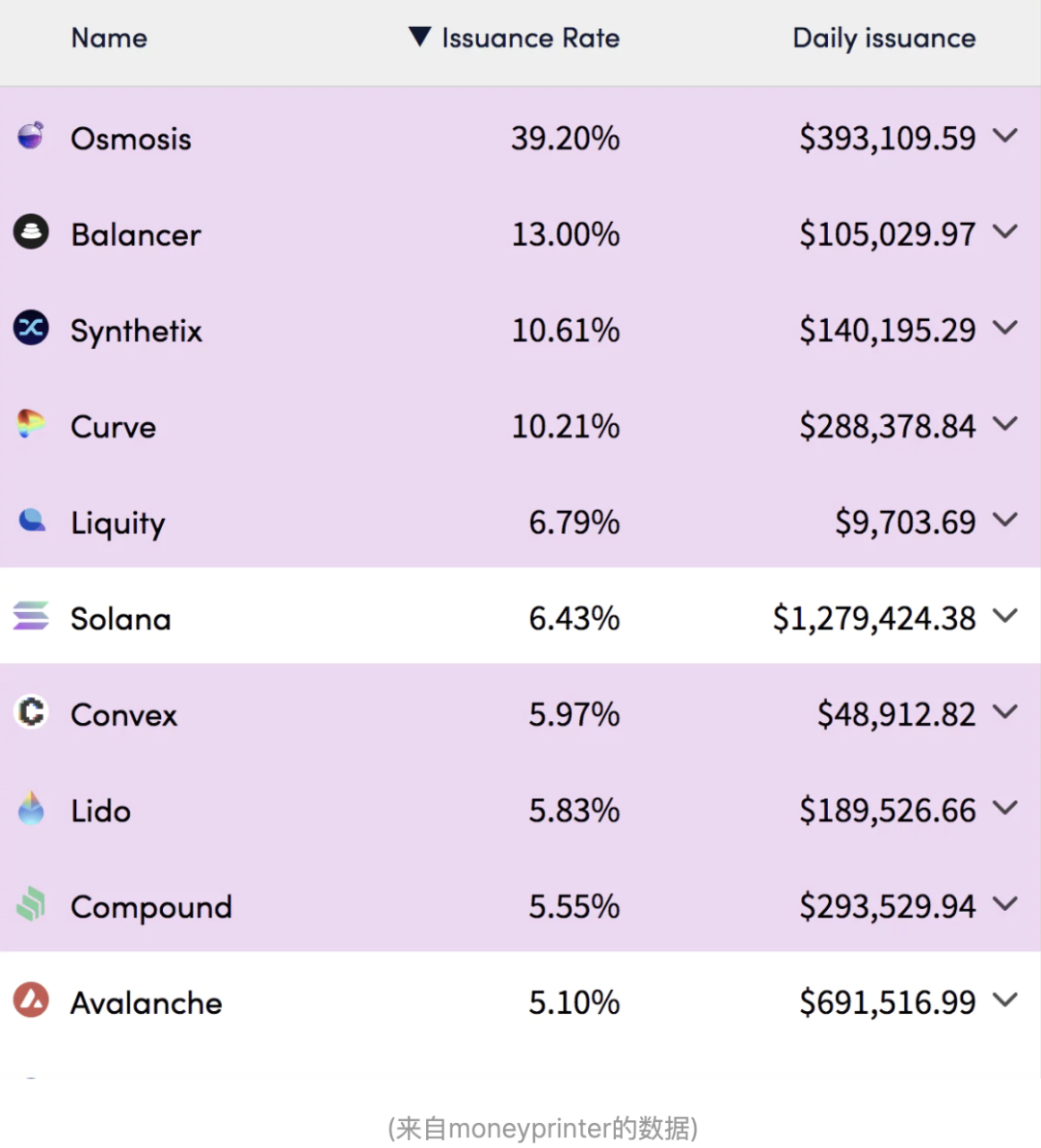

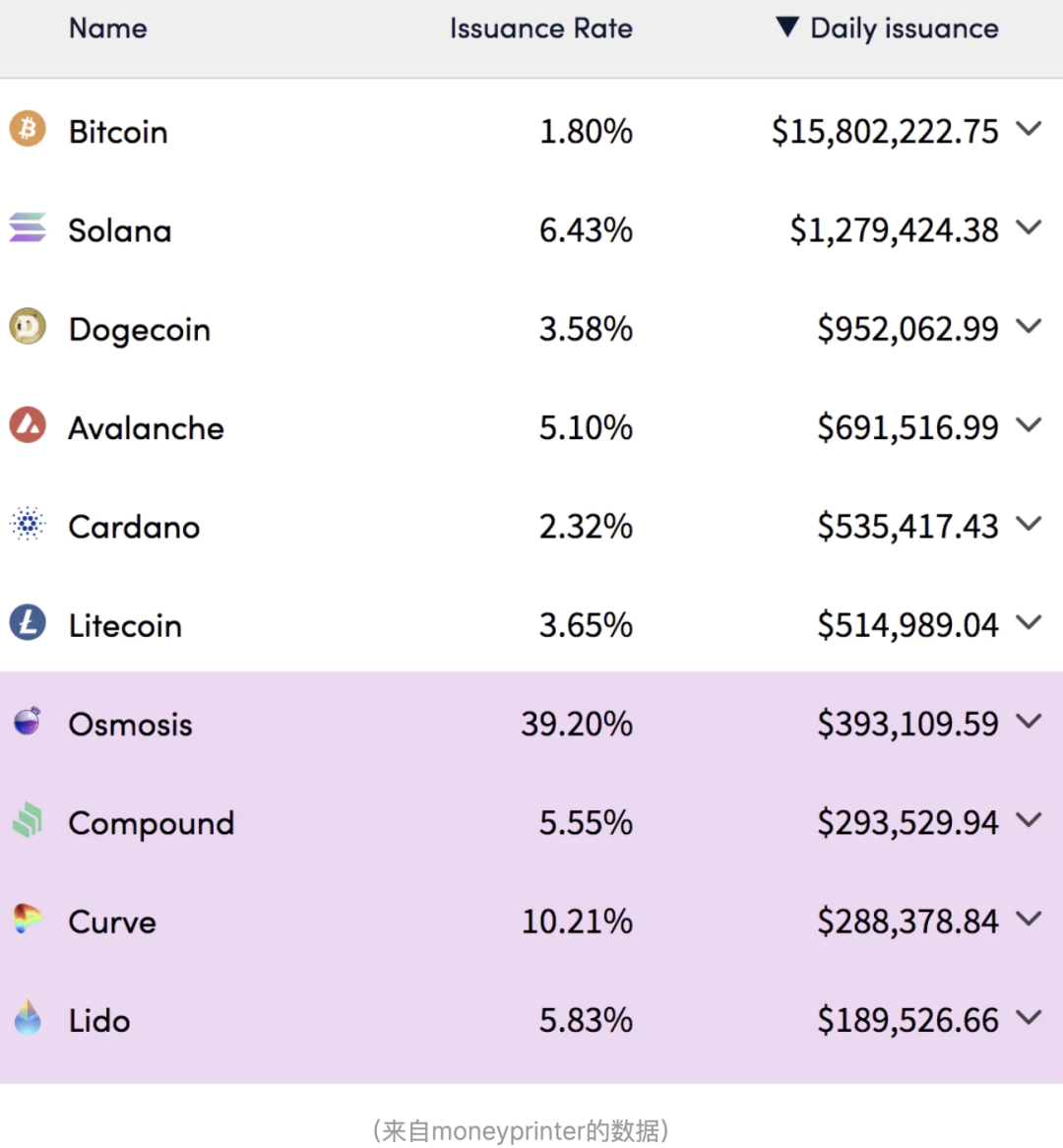

In addition, compared with other chains or projects, such as BTC, Solana, etc., the addition of ETH has been very small.

Ethereum Shanghai upgrade will generate a lot of selling pressure? Look at it from these 9 aspects

Ethereum Shanghai upgrade will generate a lot of selling pressure? Look at it from these 9 aspects

It is currently a bear market, and the gas consumption is relatively small. If the market becomes more active in the future, the daily deflation of Ethereum will also be very considerable.

As far as the current situation is concerned, ETH is much lower than other public chains in terms of new rate and daily added value, and is also much lower than BTC.

7. Community Consensus of Ethereum

Ethereum itself has a developer base, an ecological base, and a user base. Based on this, a relatively strong community consensus has been formed. This kind of community consensus, with the continuous development of the Ethereum ecosystem, including L2 gradually surpassing most public chains, Ethereum's role as the most basic settlement layer and security provider in the encryption field will only strengthen its moat. The fact that there is a sufficient moat will gradually be seen by more institutions and users.

8. ETH pledge rate of return is a dynamic game

The lower the amount of ETH pledged, the higher its rate of return; if the number of pledges drops to a certain level and its rate of return rises, it will attract people to enter. This relatively stable return will appear more attractive in a bear market. Therefore, there is also a dynamic balance here.

Ethereum Shanghai upgrade will generate a lot of selling pressure? Look at it from these 9 aspects

The Shanghai upgrade not only includes ETH pledge unlocking, but also other upgrades, which are also conducive to the long-term development of its ecology. For example, EIP-3651 can help miners save gas fees and speed up miner transactions; for example, EIP-3855 can also reduce gas consumption; EIP-3860 can support larger contracts and support the deployment of contracts with richer functions, which is beneficial for developers to launch more Imaginative dAPP; EIP-3540 (EVM Object Format EOF) V1 supports the separation of contract code and data, simplifying contract interaction, etc.

epilogue

epilogue

In general, even if Shanghai upgrades and opens the withdrawal function, the impact on ETH selling pressure is limited. As the event of Shanghai’s upgrade itself, it is conducive to the long-term development of the Ethereum ecosystem, which is considered a long-term positive event.

Finally, it needs to be reminded that although the Shanghai upgrade will not bring about a large short-term selling pressure, it is two different things from the fluctuation of the price of ETH itself. If there is a black swan event during this period, even if there is no pledge to unlock, it will have an impact on the market.