Interview: Nian Qing, ChainCatcher

Respondents: Crylipto, BendDAO co-creation

More than a month ago, as the floor price of Boring Ape continued to fall, it directly triggered a series of liquidations of BendDAO, the NFT mortgage loan agreement with the largest number of Boring Apes listed. When the words "death spiral" and "liquidity crisis" appeared, people who were devastated by the UST/LUNA incident to PTSD fell into panic again. In just a few days, the liquidity of nearly 20,000 ETH in the BendDAO lending pool almost dried up.

This liquidity crisis has further sparked bearish discussions on the NFT financial sector. Voices such as "NFTFi is starting to fail in the bear market" and "NFT lending is a fake demand" are rampant, and some even think that the fuse of the NFT market collapse. Looking back now, has the market reacted to this liquidity crisis? Can NFT loans survive this bear market?

ChainCatcher recently interviewed Crylipto, the co-founder of BendDAO. He reviewed the whole incident from an internal perspective, the role of BendDAO in the NFT market, and the needs that NFT lending is really solving.

In the interview, Crylipto mentioned that some short-term market factors such as the merger of Ethereum are easy to be ignored, but they are very critical, and the project party really needs to have such sensitivity. But for BendDAO, this liquidity crisis is also a valuable stress test.

Crylipto believes that for a truly decentralized platform, the situation facing a liquidity crisis is not the same as CeFi. CeFi may have invisible financial loopholes or hidden dangers such as embezzlement, but in the decentralized market, the death spiral caused by negative emotions, the worst result is that the pool is empty, and the impact is relatively limited.

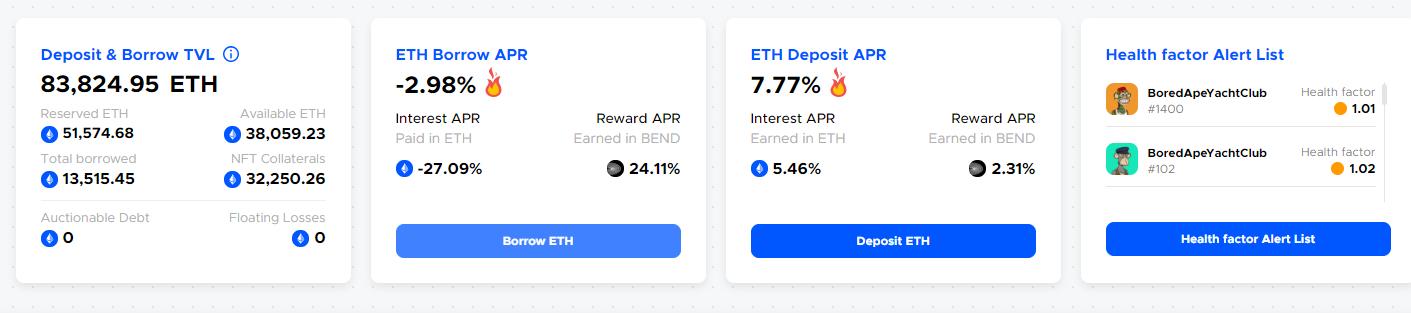

At present, the total liquidity of BendDAO's current lending pool is 51,574 ETH, the available liquidity is 38,059 ETH, the fund ETH Deposit APR is 5.46%, and the fund utilization rate is 26.21%. The platform has supported eight blue-chip NFT projects including BAYC (300), CryptoPunks (46), MAYC (247), Azuki (193), Moonbirds (2), CloneX (123), Doodles (8), and Space Doodles (8).

The following is the full text of the interview:

1. ChainCatcher: Please briefly introduce the development history of BendDAO.

Crylipto:Around July and August last year, NFT began to replace DeFi and GameFi as a trend and hotspot in the market. At that time, we also participated in the NFT craze of BAYC and CryptoPunks, bought and held, and have been paying attention to the development of NFT since then. In the process of buying and selling, we began to realize how important liquidity is to NFT transactions.

Around the same period, the co-founder and I began to think about the issue of NFT liquidity. It mainly inspected three directions: the first is the very popular NFT fragmentation method at that time, the second is NFT lending, and the third is NFT options, derivatives, etc. In the end, we chose the direction of NFT lending, referring to the Bonding Curve model of AAVE, thus establishing the development direction of BendDAO.

2. ChainCatcher: BendDAO was officially launched at the beginning of this year. It has developed into a relatively leading project in NFT lending. The progress is still quite fast. How did the team complete the traffic accumulation in a short period of time?

Crylipto:In retrospect, the logic is very simple, but the team was not very sure (whether it would be successful) beforehand. We did a lot of market analysis. At that time, there were many small lending platforms, most of which were peer-to-peer. However, the experience of GameFi and DeFi tells us that the capital efficiency of on-chain lending is very critical, and we finally chose the P-2-Pool model. Therefore, the choice of market direction in the early stage of project development is very important.

Second, we are still very close to the community. The team members themselves are the holders of BAYC and CryptoPunk, so they will share and exchange product experience with the community.

Third, BendDAO is not a new team. It is very experienced in building products, so it has put a lot of effort into product experience and security.

Also, I feel more fortunate that the product launched before the Boring Ape launched the land (Otherside) airdrop. Many Boring Ape holders will seek to buy more Boring Apes in order to receive airdrops.

3. ChainCatcher: In late August, BendDAO had a liquidity crisis due to the cooling of the NFT market and the drop in BAYC floor prices, but the community and team responded quickly to this crisis. Looking back now, what experiences and lessons can be drawn from this incident?

Crylipto:This thing is still quite interesting. Before the liquidity crisis, we actually realized that BendDAO is a two-sided market that needs to balance demand. One side is NFT holders, and the other side is ETH liquidity providers. However, BendDAO actually favored NFT holders in the early days, such as the "48-hour forced liquidation protection" set in the previous BendDAO liquidation mechanism, "the liquidator's bid must exceed 95% of the floor price at the auction" and "greater than the total accumulated debt" And other measures are from the standpoint of NFT holders to ensure that they will not suddenly find that their "beloved avatar" as a status symbol is gone after a night of sleep.

Through this incident, we realized the need to balance the needs of the two-sided market, such as adjusting the liquidation threshold from 90% to the current 80%, and canceling the 95% reserve price and first bid limit. Not only optimized the liquidation mechanism, but also adjusted the pledge rate to 10%, and then raised the first-level inflection point of the interest rate curve. More importantly, we realize that BendDAO is essentially an interest rate tool in the NFT market, and liquidity can be reasonably adjusted by interest rates.

In addition, there is a key time node in this event, that is, the merger of Ethereum. The market has a wave of short-term appreciation expectations and airdrop expectations for ETH before September 15, so some users will choose to withdraw part of their pledged ETH liquidity and store it in their wallets to receive airdrops. The team later found out in statistics that during the NFT liquidation auction, the liquidity withdrawal of about 234 ETH caused a panic, which eventually led to the "scared" away of the liquidity of about 20,000 ETH. From this we can see the asymmetry of market information.

But from our perspective, the liquidity crisis is temporary, and the crisis will naturally disappear after short-term mood swings. There are two reasons: first, DeFi projects are decentralized and transparent in nature, and the assets themselves are stored inside the contract, and there are no hidden dangers such as capital loopholes or misappropriation that CeFi cannot see; second, the appreciation of mortgage assets is still expected exist. Asset appreciation expectations are directly linked to asset quality, so we will choose blue-chip NFT projects at the beginning, and the fundamentals of these assets are all fine.

The decentralized lending market does not have problems such as regulatory friction and opacity. You can regard it as a completely free market. As long as you follow and make good use of market rules, make good use of your own leverage tools, and grasp asset quality, the long-term value of the project will It will definitely be favored. The scarcity of blue-chip NFT assets is higher than that of ETH. After the short-term crisis, the liquidity of ETH will return.

To sum up, here are some experiences: First, the lending agreement essentially matches ETH liquidity providers and NFT holders, and there is indeed rigid demand in the market. In this process, efficiency comes first Second, security is the most important thing. As long as a protocol is safe, its value will be rediscovered by the market; third, it is difficult to avoid event-based short-term fluctuations in the market, and project parties need to identify or prevent them in advance. For example, on the eve of the merger of Ethereum, AAVE also made some emergency measures (reducing the ETH borrowing limit, increasing the Ethereum borrowing rate, etc.).

4. ChainCatcher: Protocols such as JPEG'd set up a priority liquidation mechanism for the DAO treasury, that is, the DAO treasury will first buy the liquidated NFT and then dispose of it. BendDAO currently belongs to the liquidator mechanism. Have you considered diversifying the liquidation mechanism? For example, DAO participates more or introduces third-party liquidators.

Crylipto:In the past, BendDAO was basically involved in liquidation by individuals. However, after the last liquidity crisis, some professional clearing institutions are actively contacting us and getting involved. Of course, it is difficult to distinguish between institutional addresses and personal addresses on the chain, and it is difficult for ordinary users to know.

In addition, the community also realized that the treasury needs to have some funds reserves to participate in liquidation, so as to support ETH liquidity providers. . Based on this starting point, the community startedproposalAnd discuss to do a part of Token financing, and keep this part of liquidity in the treasury for the auction of non-performing assets in emergencies (in late September, the community proposed to sell 1 billion tokens of BendDAO to raise about 8 million US dollars to create An investment fund with a post-money valuation of $80 million. If approved, the fund will serve as a sub-pool of NFT lenders with at least 50% of funds invested in distressed assets). Currently, this proposal is being promoted by the community and supported by the team, and is still being discussed and revised.

But objectively speaking, community promotion is actually quite difficult. Although many organizations now call themselves "DAO", in essence it is still a small team that has the final say behind the scenes. BendDAO hopes to take a very substantial step in governance and make it a very pure DAO. However, this requires each of the community, developers, and the market to have sufficient influence and professionalism to achieve a balance among the three parties.

Of course, there will be some unreasonable and inefficient situations in this process, but this kind of discussion is the way of growth with the least cost, which cannot be avoided by the growth of the community.

5. ChainCatcher: The roadmap shows that in the fourth quarter, BendDAO plans to build P2P lending and private lending pools. What are the considerations for these proposals?

Crylipto:The goal of BendDAO is to improve NFT liquidity. Our slogan is "Web3 data liquidity". To get closer to this goal, we need to continue to deepen. At present, we have only optimized the liquidity of blue-chip NFTs, which is far from enough. After all, blue-chip projects only account for a small number of them. Therefore, in order to take care of the liquidity of long-tail NFT, we plan to build P2P lending and private lending pools in the future.

6. ChainCatcher: How do you view the several modes of the NFTFi track, such as Peer to Peer, Peer to Pool and AMM modes?

Crylipto:Macroscopically speaking, each model actually has its own demand space and usage scenarios. NFTFi is in the early stage, and everyone is still exploring in different directions, but in the final analysis, it is all to improve the demand for NFT liquidity. I think at least for now Speaking of which, there is no definitive conclusion on which is better, but only that there are some horizontal and vertical comparisons.

For example, in terms of capital efficiency, the efficiency of the capital pool (Pool) is the highest, because there is no need to wait for the matching of borrowers and lenders. However, in the coverage of NFT categories, especially non-blue-chip assets, the peer-to-peer model will have stronger advantages, because both borrowers and lenders negotiate interest rates and measure risks on demand, and the platform side only acts as a matching role, but the efficiency will be relatively low.

The AMM model actually takes into account both efficiency and long-tail NFT, but the distinction in terms of asset rarity is still relatively lacking, because NFT assets with different rarities are artificially grouped together and placed in the same Curve. This model does not do enough for the segmented pricing of market assets.

Each method has advantages and disadvantages, and NFTFi will continue to evolve, and I believe that each company will launch better iterative solutions on its own basis. This is also the most attractive part of the market.

7. ChainCatcher: What is the recent strategic focus of BendDAO? What is the long-term development plan for the future?

Crylipto:At present, the team is more concerned about the rights and interests of NFT holders. How to ensure that they can also enjoy the rights and interests of airdrops and whitelists while mortgaging NFTs. For example, we are trying recentlyBend-Ape StakingProducts, this can be regarded as a recent strategic innovation.

In terms of long-term development planning, in addition to constantly improving the liquidity of NFT, BendDAO also hopes to contribute to the practicality of NFT (NFT Utility) and creator economy, not just making NFT a financial transaction assets.

8. ChainCatcher: There is a view that NFT-Fi essentially adds a set of leverage to NFT, which can play the role of "icing on the cake" and increasing liquidity in a bull market, but when the market cools down, it will also face liquidity. The crisis of sexual insufficiency, some people even think that NFT-Fi is a pseudo-demand. How do you feel about such views?

Crylipto:In fact, you can clearly see the real needs of users on BendDAO, and the statement of "pseudo-demand" is self-defeating. We have been emphasizing that BendDAO currently only solves half of the liquidity needs, especially to make up for OpenSea’s lack of liquidity, and participate in NFT transactions through the lending pool model to release more ETH. However, after NFT is transferred to BendDAO, it also faces the liquidity problem of the auction. At present, the team is also optimizing this part of the liquidity, and there will be further planning in the later stage to better complete a closed loop of NFT liquidity.

From the perspective of the entire NFTFi, NFT, as an asset on the chain, is very close to real estate, with both practicality and financiality. The value of the NFT lending fund pool model to the NFT industry is somewhat similar to the value of the Federal Reserve to the entire financial industry. The Federal Reserve can control the liquidity of the currency through interest rates and affect the demand of the macro market, thereby promoting innovation in the entire industry.

What BendDAO is doing is actually a bit like a miniature version of the interest rate tool platform. It is very objective to release liquidity through interest rate tools, and to further stimulate the creator economy and NFT demand through the release of liquidity. Since the Federal Reserve broke away from the Bretton Woods system and independently regulated the credit currency, the United States has experienced wave after wave of technological innovation, all of which have been verified by the market.

9. ChainCatcher: What are the main aspects of the current scarcity of NFT infrastructure?

Crylipto:We can think of NFT as a concretization of users on the chain, whether it is an avatar, GameFi NFT or Pass. In the early days, users were just "a string of addresses + the balance under the address", that is, Token as a Balance. This form is very abstract, we have no way of knowing whether the address is a robot or a person, but when the address on the chain starts to have NFT, we can find out the aesthetics of this person through these small pictures, and even infer it by watching him buy Punk and monkeys This user is OG.

This is similar to the early days of Internet development. At that time, there was a joke that "you don't know whether you are chatting with a human or a dog", because everyone is anonymous or semi-anonymous, until the avatar, status, signature, personal space, information wall When it appears, we can see whether the person opposite is a beautiful girl or a big guy who picks his feet. It has evolved to a real name now. Therefore, NFT is actually assisting the users behind the blockchain network to develop in this direction, which is also in line with people’s social needs. SocialFi, GameFi, etc. are all developing in this direction, but the network must carry people’s social interaction. capacity required.

Jobs once said in an interview in his early years: "The current bandwidth is not enough to convey emotions. To convey emotions, you need more bandwidth. Most people do not have such high-speed bandwidth, and most online content is also emotionless." From this perspective Speaking, the infrastructure of NFT is to allow everyone to present the personality on the chain on the blockchain network. Vitalik once proposed Soulbound Token (soul bound token). In this context, Token as a Balance will become NFT/Token as Service, so that NFT can be used as a service to record activities on the chain.

This requires NFT to have strong interactivity and the ability to express personality, which has additional requirements for the underlying infrastructure, which is far from being met by the current blockchain. Take Ethereum as an example, NFT is passively bound to the address on the chain as a static image resource file through the interface. But any input of this small picture is not accepted on the chain and will be ignored. The most fundamental reason is that the chain cannot meet these interactive needs with the lowest cost, and further evolution is needed. At present, the Move language used by new public chains such as Aptos and Sui has actually taken into account the interactivity of NFT.