Original author:CryptoJoeOriginal author:

(Founder of Rebirth DAO, senior trader)

Original compilation: czgsws, BlockBeats

stETH unanchored and dropped to 0.95 ETH in value.@Riley_gmiBeen researching this a lot lately, and here are some of our findings.

first level title

First of all, what is Lido & stETH?

Lido provides users with ETH liquidity staking services, users can lock any amount of ETH, and then receive the equity Token stETH to earn income in DeFi.

After the merger, each stETH can be exchanged for 1 ETH normally.

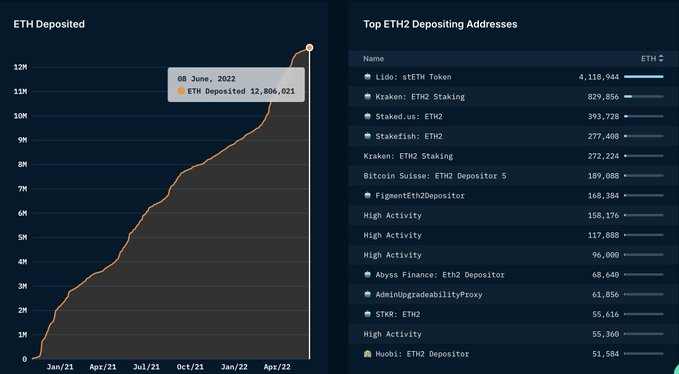

Each stETH can only be redeemed through the launch of the beacon chain. Until then, the 12.8 million ETH in the ETH 2.0 staking contract is illiquid.

Lido holds 32% of the 12.8 million ETH (about 4.1 million)

Before we dig into Celsius' balance sheet and track down Smart Money addresses, let's see how stETH should be priced:

But how much of a discount to the price of stETH is fair given the liquidity dynamics of this investment?

first level title

StETH pricing should be determined by a combination of the following 4 things

· Current market desire for liquidity (demand/supply)

· Current market volume and liquidity (how the market is responding to selling pressure)

· Likelihood of a successful/delayed merger

In detail

secondary title

1. Desire for market liquidity

During different phases of the market cycle, the need for liquidity ebbs and flows. When the price rises and the liquidity is high, it is easy to close the position and the cost is low, and vice versa.

Through the data on the chain, we have seen a large number of withdrawals of stETH, such as the encrypted financial service provider Amber, whose wallet address has withdrawn stETH worth more than 140 million US dollars from the Curve pool.

This has been an increasing trend over the past few days and may indicate that a larger potential sell-off is brewing.

In this case, the most critical supply and demand side is looking at the encrypted lending platform Celsius. If anyone believes that Celsius may be forced to sell a large amount of stETH, then this will greatly change the supply and demand relationship we emphasized earlier.

So what is the liquidity of stETH?

secondary title

2. Current market volume and liquidity

Early this morning, the total liquidity in the pool dropped by over 20%, there was a massive sell off of wallets related to Alameda Research, and Celsius also mentioned this before I posted these.

Amber's withdrawal of more than $150 million in stETH liquidity is significant and likely only an early warning of a sell-off.

That's $150 million, and it's likely to hit the market in the next few days.

The second point is that the liquidity pool on Curve has become extremely unbalanced, which is dangerous and will greatly increase the risk of decoupling.

The withdrawal of liquidity from 3pool on Curve was the first shot that caused UST to crash. Less liquidity = more risk.

Those stETHs entering the market could deal a major blow to the market.

secondary title

3. Likelihood of a successful/delayed merger

In this sense, if the merger is delayed, and it takes 6-12 months to get back the ETH after the merger, then locking the Token will increase the liquidity cost, which is far greater than the benefits obtained during this period.

secondary title

4. Smart Contract Risks

Demand/liquidity/consolidation risk aside, there is also smart contract risk.

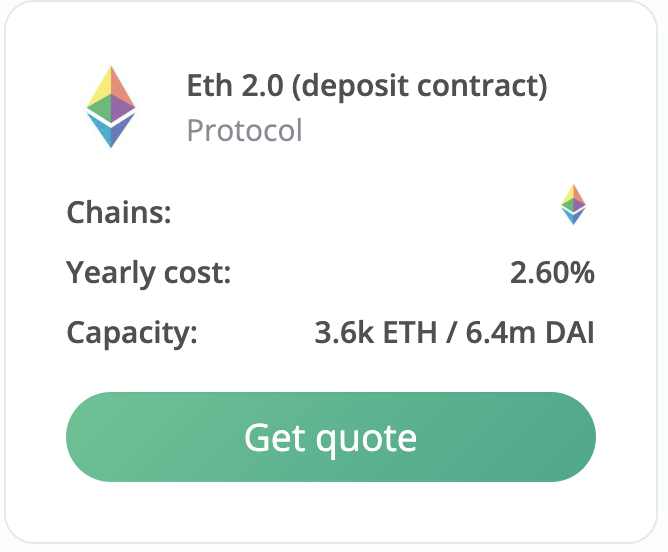

Based on the insurance cost of the Lido deposit contract on Nexusmutual (2.6%), pricing is straightforward.

Therefore, the smart contract risk ALONE in stETH is at least 2.6%, which is roughly the current discount of stETH/ETH.

This shows that the risk of stETH is seriously underestimated.

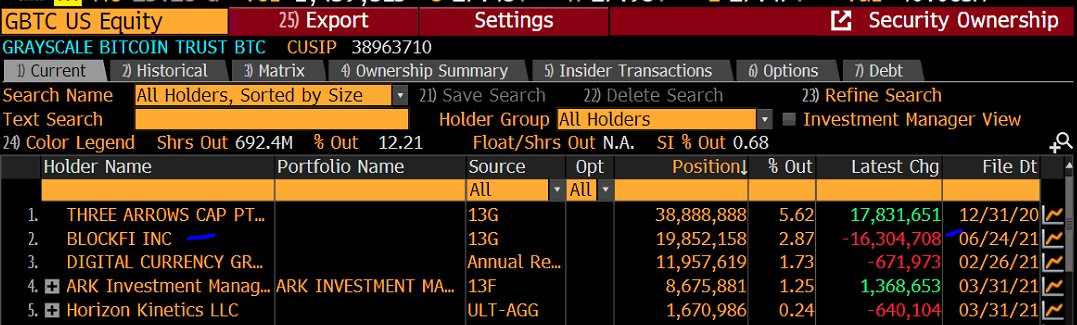

A similar case to how stETH is priced is GBTC, as they are both closed.

If you want to sell your GBTC position, you have to sell it on the secondary market because it is a closed-end fund. Before it was converted to an ETF, the secondary market was the only option for liquidity.

If you want to sell your stETH, you have to sell it on the secondary market until the merger.

In both cases, this liquidity, open-ended risk, and supply-demand dynamics are the underlying factors that affect the market's fair value for that asset.

But in this case, why is one trading at a 3% discount and the other at a 30% discount, not to mention the fact that stETH has Lido's smart contract risk.

Lido's 7 investors created a similar situation to UST, they are a16z, Alameda Research, Coinbase, Paradigm, DCG, Jump Capital and Three Arrows Capital.

Similarly, Blockfi, one of the largest holders of GBTC, currently has a floating loss close to more than $500 million.

This has been reflected in Blockfi's valuation, BlockFi is raising a new round of financing at a valuation of $1 billion, and in March 2021 their valuation was $3 billion.

What's the point? Many of the big players in the game are often wrong and in this case completely miscalculate the liquidity cost of GBTC and stETH, both of which are liquidity black holes in this case.

So in the end, we believe that the one-year staking yield for this liquidity trap is too low.

Perhaps the figure should be similar to GBTC at 30%, but not 3%.

Now, let's see what's happening in the market right now:

Liquidity is exhausted, whales and smart money are selling.

The amount of stETH held by smart money addresses dropped from 160,000 stETH to 27,800 stETH within 1 month.

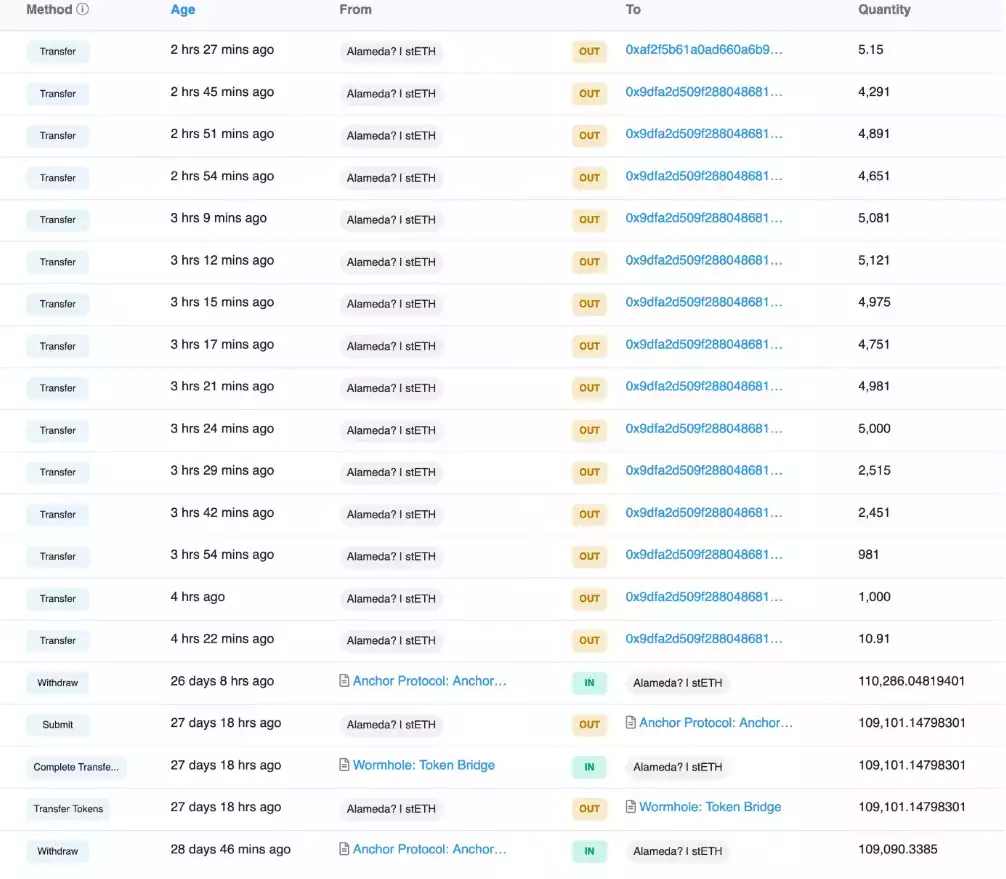

In fact, Alameda dumped 50,615 stETH into the market within 2 hours this Wednesday.

It is quite possible that someone deliberately pulled the anchor towards the liquidation price of stETH.

Leveraged stETH holders risk being liquidated if they do not have sufficient collateral.

For example, at stETH=0.8 ETH, $299 million will be liquidated.

The emphasis here is on the short term. I ultimately believe people will be happy to buy stETH at a discount. However, when some institutions have to sell, the situation will change slightly.

The institution that may have to sell is Celsius.

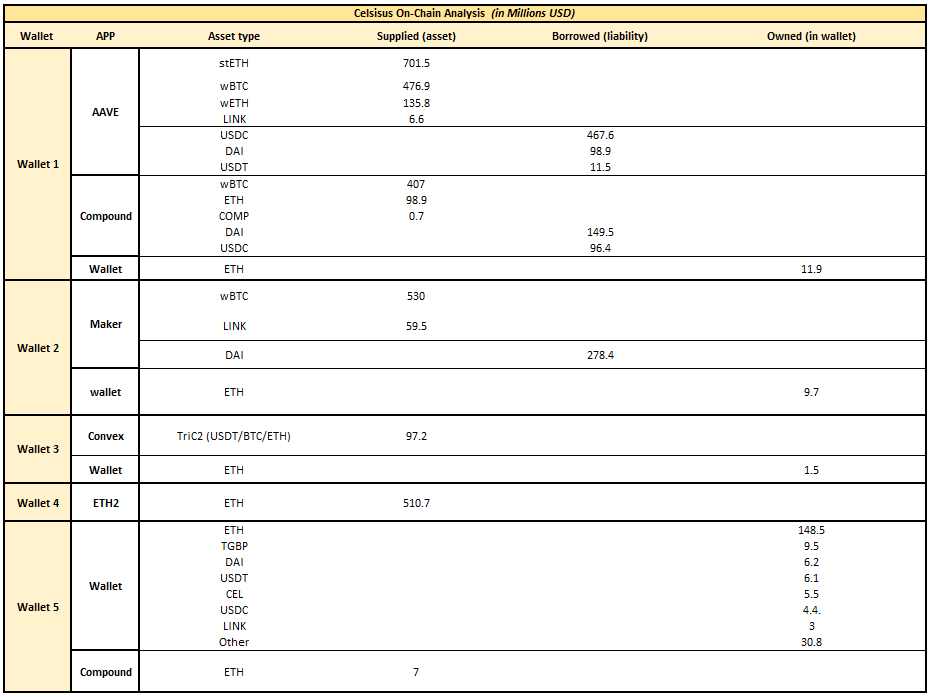

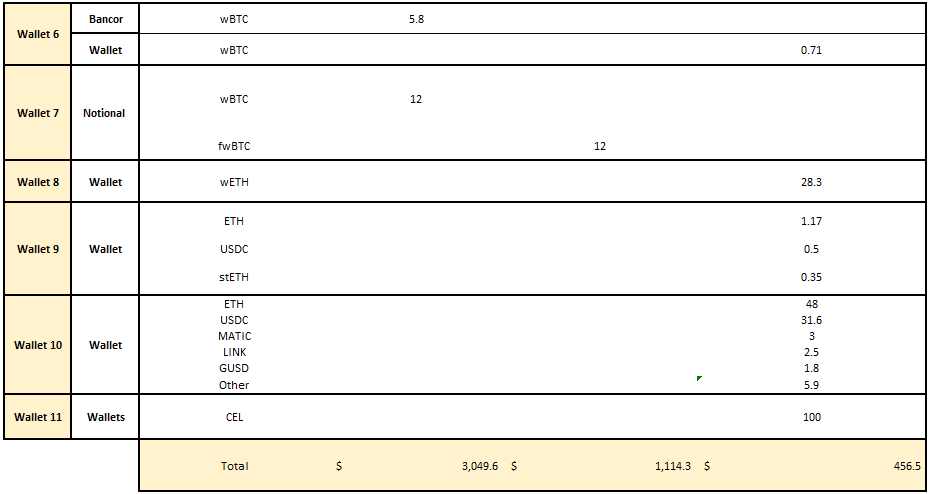

By performing an on-chain analysis, I was able to calculate Celsius' assets and liabilities.

Total assets are $3.48 billion, loans are $1.11 billion, and net assets are $2.374 billion (assuming Celsius holds 45% of its CEL Token supply, worth about $100 million).

A full breakdown of the assets held is as follows:

*Note, this is only their assets in DeFi, no one knows what crypto assets they hold elsewhere (such as in CEX).

They claim to have a TVL of about $10 billion, but that's all I can find.

The important part here is that Celsius is the whale holder of stETH. In fact, they are the largest interest-bearing stETH holders (on AAVE).

If we analyze Celsius's ETH holdings specifically, we find that 71% of holdings are illiquid or low-liquidity types.

$510 million in ETH is locked in the ETH2.0 staking contract and cannot be withdrawn until after the merger.

$702 million is in stETH, which cannot be easily exited through liquidity pools.

What happens if Celsius users want to redeem their money?

Are they redeeming?

Why did they activate "HODL Mode" on their account?

On October 8, 2021, Celsius reported that its AUM exceeded $25 billion. Celsius is a private company and has only released its financials for 2019 and 2020, and despite repeated calls from investors on various social platforms for them to release new financials, they did not for 22.

The company also did not issue an audit report. They did it in '19 and '20, but not in '21.ChainanalysisOn 12/20/21, they communicated with

The partnership released a report confirming that since its launch in 2018, users have deposited more than $7.609 billion on the platform and withdrawn more than $4.29 billion.

According to the report, Celsius had $3.31 billion worth of on-chain assets on Dec. 20.

The company reported administrative expenses of $35 million, 40% higher than cost of sales.

The lack of transparency has investors concerned about the possibility of a run on Celsius.

The company currently holds debt on stablecoins, rather than holding positions in ETH, BTC, and LINK, which exposes them to market risk of downward cryptocurrency prices.

If the market crashes, they will face a debt crisis.

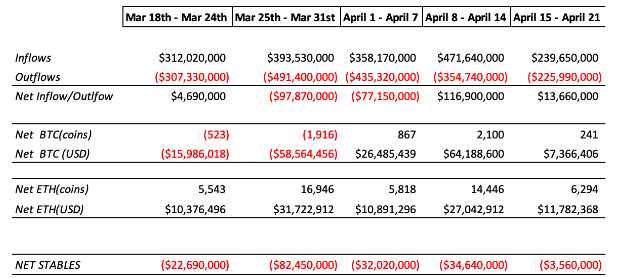

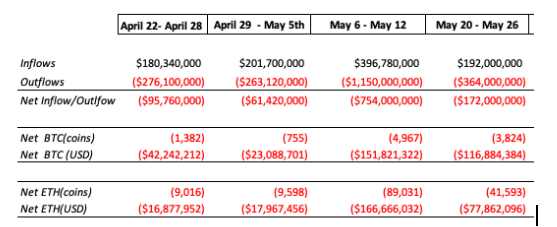

After Terra crashed (May 6-12), there was an outflow of $750 million (150 million ETH and $150 million BTC).

The company had a net outflow of $450 million in the last two weeks of May.

Even if we ignore the week in which no outflows were reported, Celsius experienced a total of $1.2 billion in outflows.

Such outflows increase the risk of a run on Celsius.

The chart below shows outflows over the past 5 weeks. Total withdrawals over the past 5 weeks are 190k ETH.

Compared to the previous 5 weeks when Celsius had 50k inflows.

Celsius has been experiencing massive divestments of ETH and assets in general.

Currently, they have enabled "HODL Mode" which prevents users from withdrawing funds from Celsius.

Another problem with Celsius is that only 29% of Celsius’s ETH is liquid:

1. Liquid ETH

Most of the ETH is deposited into AAVE (150k ETH) and COMP (45k), both positions are collateralized by ~45% LTV of assets.

They have to pay off the loan before they can withdraw their ETH.

2. 458k of ETH in StETH

In the liquidity pool on Curve, st-ETH and ETH are highly unbalanced, with only 250k of ETH paired with 642k of stETH. If Celsius were to exchange all St ETH, they would only get 250k ETH.

3. 324K ETH has been deposited into the ETH 2.0 contract, Celsius will not be able to obtain these ETH for at least 1-2 years

- 158K of which were obtained through Figment.

- The remaining 166,400 are obtained through the Ethereum Foundation ETH 2.0 contract.In addition, they are。

$70M Lost in Stakehound Event

(BlockBeats Note: On June 7, according to Dirty Bubble Media, the encrypted lending platform Celsius Network lost at least 35,000 ETH in the Stakehound private key loss event.)$50M Lost in BadgerDAO Hack。

besides,$500 million in customer deposits wiped out in recent LUNA crash。

first level title

So how do you trade to profit in this situation?

We've thought about it and reached out to market makers, and we've scoured DeFi. You need to find a place to borrow stETH before you can sell it, and there is no relevant contract, so it is a bit difficult to make money from it.

There are two main ways to do this.

1. The over-the-counter market.

If you are a large institutional player, you will have access to market makers and brokers who can lend you stETH against your ETH collateral.

2. Euler finance

This is impossible for 99% of market participants.

You can deposit ETH at 4% holding cost and borrow wstETH to sell on Curve, Uniswap or 1inch.

The profit/loss ratio of the transaction is very good, because the biggest cost is that ETH is back to anchor, and you have to repay the loan; this is about 5-6% loss.

Similar to UST, this is an inexpensive way to bet on the market given the limited upside risk of stETH valued more than 1:1 with ETH.

Another way to profit from this trade is to buy stETH at a discount. If stETH is trading at a bigger discount than GBTC (30%), and there are institutions in the market that must sell (such as Celsius or others). To us, this feels like a great opportunity to convert any ETH holdings into stETH.